Business Day

Bloated Pay Came

Before Hain Celestial’s Error

Fair Game

By

GRETCHEN

MORGENSON

AUG.

19, 2016

|

The Hain Celestial Group is a

maker of natural and organic foods and beverages.

The Hain Celestial Group,

via PR Newswire

|

|

The Hain

Celestial Group is a maker of natural and organic foods and beverages.

Credit The Hain Celestial Group, via PR Newswire

The Hain

Celestial Group, a maker of

natural and organic foods and beverages,

has been riding high in the market. But on Monday it came crashing to

earth when it disclosed an accounting problem, delayed its full-year

financial report and said it probably wouldn’t meet its earnings

guidance for 2016.

Investors have

dumped shares in the company, based in Long Island, wiping out $1.5 billion in

market capitalization.

The problem, Hain

said, was that it might have improperly recognized revenue from certain

distributors in the United States during an unspecified period. The company,

which says its purpose is “to create and inspire a healthier way of life,” may

have mistakenly recorded revenue when it shipped products to the distributors,

rather than waiting until those goods had been sold to consumers.

Not the most

transparent disclosure in history, that’s for sure.

Hain said it did

not expect the accounting problem to have an impact on the total amount of

revenue the company had recognized, but it said it was assessing its internal

controls over financial reporting.

Clearly, investors

were stunned by Hain’s statement. Maybe they shouldn’t have been.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

According to corporate governance experts, clues to oversight problems

at Hain have been evident for a while in its excessive executive pay

practices and disdain for shareholders’ anger about them.

“When

you see overcompensation, it’s usually indicative of failure in other

areas,” said

Charles Elson, director of the

John L. Weinberg Center for Corporate Governance. “Compensation is

oversight. It’s a picture window into the boardroom because it’s such

an important issue.”

Hain is led by Irwin D. Simon, who founded

the company in 1993 after stints at the SlimFast Foods Company and Häagen-Dazs,

the ice cream maker. He wears three hats at Hain: president, chief executive and

chairman of the board.

For a founder, Mr.

Simon does not own that many shares of Hain. As of February, he held 1.9 million

shares, or 1.8 percent of its stock outstanding. Those holdings are worth about

$74 million at current prices.

Unlike some

company founders, who eschew high pay, he has enjoyed hefty remuneration that

comes from shareholders. Over the most recent three years — fiscal 2013-15 — he

has received an average of $18.1 million in annual compensation.

That is a bounty

for a company of Hain’s size, which reached $2.7 billion in sales for the most

recent fiscal year.

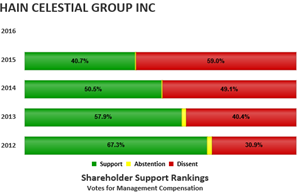

What is more, many

of Hain’s shareholders have expressed their

displeasure with the compensation, voting in

nonbinding resolutions against the company’s pay practices in higher numbers

with each passing year. In 2012, for example, 30.9 percent of votes cast at

Hain’s annual meeting were nos. By 2015, this figure had risen to a staggering

59 percent.

This is a striking

contrast to the 5 percent median nay vote tallied at all 500 companies in the

Standard & Poor’s index this year.

Mary Celeste

Anthes, a Hain spokeswoman, said in a statement:

“Hain

Celestial is committed to delivering value to all of our stakeholders and has

created significant value for our stockholders over time. We have a very strong,

experienced and highly independent board that exercises its oversight role with

great care and diligence as evidenced by the fact that we self-identified and

have begun to review the potential accounting issue through our internal

examination and the oversight process led by the audit committee and independent

external counsel.”

Among Hain’s

institutional holders that have voted against its pay is Vanguard, the company’s

second-largest holder. By contrast,

BlackRock, Hain’s biggest shareholder, voted

its investors’ shares in support of Hain’s compensation at the 2014 annual

meeting, the most recent year for which a breakdown by shareholders is

available.

Last year, the

company tweaked its compensation in response to the shareholder fury. Hain said

it would extend the pro-rata vesting period for restricted stock grants to three

years from two, increase the proportion of equity compensation to cash and “seek

to eliminate” the double dip in pay that resulted from its use of identical

performance metrics in two incentive plans.

Judging by the

numbers, Hain shareholders viewed these changes as too little, too late. After

they were announced, the company received its highest negative vote on pay.

“Obviously, their

compensation consultant told them to give investors a few things,” Mr. Elson

said. “The fact that they’re now listening, albeit a little bit, is a good

thing. But when you get into high double digits on pay votes, a board that

ignores that is making a terrible mistake.”

The pay of Hain’s

chief hit my radar screen three years ago when Equilar, a compensation analysis

firm in Redwood City, Calif., identified

problems with the peer groups the company

used for pay purposes.

Many companies

benchmark their pay against a group of companies in their industries. Most of

Hain’s chosen peers had higher revenue than the company and half had larger

market capitalizations, Equilar found. After Hain tilted the playing field in

its favor, Mr. Simon received far more than the median pay awarded to chief

executives at those larger peers.

Ms. Anthes said

the company’s changes to its pay programs were made in consultation with its

stockholders and corporate governance experts; the modifications “respond to

their input and clearly align pay with performance,” she added.

It is unclear when

Hain will produce its full-year financial results. Having identified the

accounting error, it said it would issue its scrubbed report as soon as

possible.

But the accounting

problem isn’t likely to improve its relationship with shareholders. Their anger

may boil over at its as-yet-unscheduled annual meeting this fall.

Even before Hain’s

recent problems, three of its directors came under fire from shareholders. They

are the members of its compensation committee: Richard C. Berke, a former

executive at Broadridge Financial Solutions, an outsourcing provider; Scott M.

O’Neil, chief executive of the Philadelphia 76ers and the New Jersey Devils; and

Adrianne Shapira, chief financial officer of David Yurman Enterprises, a

designer jewelry maker, and a former equity research analyst at Goldman Sachs.

At last year’s

meeting in November, more than one-third of the votes cast withheld support for

the three directors. That kind of dissent is rare in the boardroom.

Through the Hain

spokeswoman, the directors declined to comment.

Hain characterizes

itself in its filings as a leader in corporate governance that has “consistently

demonstrated our longstanding willingness to listen and respond to our

stockholders’ concerns.” Really?

Shareholders of

United States companies are a pretty easygoing bunch most of the time. It

typically takes a lot to get them agitated. But when they do protest, corporate

board members should know better than to ignore them.

A version of this article appears in print on August 21, 2016, on page

BU1 of the New York edition with the headline: Bloated Pay Came Before

Hain’s Error.

© 2016 The

New York Times Company