Institutional Investor Survey 2021

Posted by Kiran Vasantham, Jana Jevcakova,

and Mandy Offel, Morrow Sodali, on Sunday, June 6, 2021

Executive

Summary

We are

delighted to publish Morrow Sodali’s sixth annual Institutional Investor Survey

(IIS), which canvasses the views and opinions of more than a quarter of the

world’s assets under management [1] at

a globally significant point in time.

Against the

backdrop of the COVID-19 pandemic, Environmental, Social and Governance (ESG)

impacts at listed public companies have been propelled to the forefront of

investors’ minds as they assess the management of risks and opportunities,

operational resilience, and shareholder value creation through a period of

unprecedented market uncertainty and turbulence.

As is widely

reported, the trend of capital inflows into ESG-oriented investing has exploded

reaching a record high of USD 1.65 trillion in 4Q2020, up almost 29% from the

third quarter. [2] The

COVID-19 pandemic has contributed to the acceleration of ESG investing.

Importantly, the pace of investment in sustainable funds is expected to continue

to increase in the race towards a net zero carbon economy by 2050.

For this

reason and following a global health crisis, the interest and appetite of

investors, especially asset owners, to hold boards and companies accountable for

their performance against “nonfinancial” ESG criteria is set to match, and in

some cases exceed, performance against traditional financial measures.

Therefore,

understanding and thoughtfully responding to the concerns that are weighing on

the minds of investors, it is necessary now more than ever to build investor

trust and support as companies and their leaders are faced with navigating

unique challenges. We hope that the findings of our IIS 2021 contribute to that

objective.

It should not

come as a surprise that over the past year, COVID-19 was identified by our

survey as one of the top reasons prompting investors to engage with companies.

With the mounting economic and operational pressures caused by the pandemic,

investors and other stakeholders are asking companies to articulate their

“Corporate Purpose”, mission and values as a core part of how they conduct

business.

Compensation

to senior executives has also come under specific scrutiny as a result of the

pandemic. Investors require cogent explanations where incentives have been paid,

especially if government “handouts” have been taken and where financial

performance has suffered. This scrutiny will continue into 2021 as company

revenues and profitability continue to be affected by the pandemic.

We note that a

number of identified survey trends over the past few years have continued,

including investor preference to engage directly with the board on environmental

and social issues. Undeniably however, investors rank climate risk as the most

important ESG issue and engagement topic for the second year running. Expanding

on data gathered from last year, investors are particularly interested in

understanding ESG in the context of a company’s business plan and the

identification of clear connections to financial risks and opportunities in a

company’s climate-related disclosures.

The growing

importance of climate risk has now clearly translated into investor willingness

to hold companies and boards accountable through the filing and co-filing of

ESG-related shareholder resolutions. This notable shift in attitude marks a

turning point in the relationship between companies and shareholders where the

failure of polite dialogue to drive change will directly impact investment and

voting behaviours.

Interestingly

many investors stated to be in favour of a “Say on Sustainability”. While a

number of companies worldwide have voluntarily adopted non-binding “Say on

Climate” voting resolutions, the survey suggests that in the near future “Say on

Sustainability” voting resolutions may also be on the table. However, in terms

of a “Say on Climate”, there are notable differences depending on the region; on

the one hand a number of European, Canadian and Australian corporations have

been open to the idea, but on the other, there has been significant push-back

from US companies and investors. It goes to say that similar differences could

be expected concerning any future “Say on Sustainability” campaigns.

These, and

other findings and insights can be found in our IIS 2021.

Finally, we

would like to sincerely thank all institutional investors who gave their time to

contribute to this survey.

About the

Survey

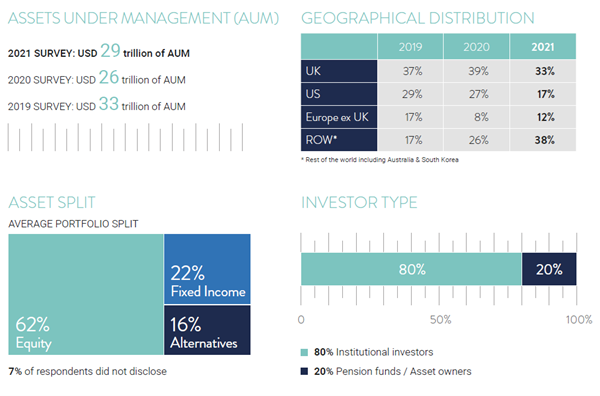

For the IIS

2021, a total of 42 global institutional investors, managing approximately USD

29 trillion in Assets Under Management (“AUM”) voluntarily participated in the

survey. The data is therefore representative and can be extrapolated across the

total global investable universe.

Responses were

gathered from direct conversations or via an online survey. Participating

investors represented a diverse spectrum of funds in terms of investment style,

profile, size and geographical location, among other attributes. The data and

findings will therefore be of interest to a wide range of listed companies

across all sectors, boards of directors and other capital market stakeholders.

To enable

year-over-year comparisons, a number of survey questions are repeated or follow

similar themes. In addition, new questions are asked that reflect topical

developments and themes.

Our Commitment

to the Company-Investor Relationship

We carry out

this survey to find out what is really important to investors when analysing

companies.

We conduct

this annually at our own expense because we are committed to enhancing the

relationship and understanding between companies and investors. It also informs

our work helping client companies with shareholder engagement and a broad suite

of corporate governance services. This also supports company-investor relations

that can be made more fluid, efficient, and effective; companies know what to

focus on and investors receive the information they need.

Ultimately

what underpins Morrow Sodali’s activities is facilitating dialogue and

understanding between companies and their institutional shareholders so they can

achieve the best outcome possible. This survey forms part of that endeavour.

Key Findings

A total of 19

survey questions were asked across four categories:

-

Company Engagement

-

ESG & Sustainability

-

Remuneration and Voting

-

Shareholder Activism

Anecdotal

feedback and opinions were also invited and analysed as part of the survey

findings and observations as outlined in the table below:

A. Company

Engagement

-

Investors are giving ESG

more focus when engaging and investing, and a significant majority are taking

ESG into greater consideration when voting.

-

Key drivers for increased

ESG focus are the links to financial performance, followed by legislative

changes and client interest.

-

Investors cite the

discussion of ESG in the context of a company’s business plan as the key basis

for effective company engagement.

-

Climate risk remains the

number one engagement priority closely followed by human capital management,

remuneration and board composition. COVID-19 was also a top engagement

priority as were cybersecurity and supply chain management.

B. ESG and

Sustainability

-

Climate change is very

important to the investment decision-making process.

-

Every surveyed investor

reviews a company’s climate-related disclosures.

-

The top three improvements

investors are seeking from climate-related disclosures are clear links to

financial performance, the time horizon to impact on strategy and the

disclosure of metrics, targets and achievements.

-

Companies are expected to

disclose their “Corporate Purpose”, and engagement with the board was given as

the top action in the absence of disclosure.

-

TCFD was overwhelmingly

the most popular ESG reporting framework, followed by SASB and then in-house

proprietary frameworks focused on material topics.

-

Many investors support an

annual “Say on Sustainability”. However, there are also many who consider the

option to vote against the reelection of directors as sufficient to make their

voices heard on this topic.

C.

Remuneration & Voting

-

ESG factors should be

considered when designing executive remuneration plans.

-

For both short and

long-term incentive plans, a weighting for ESG metrics and targets between 5%

and up to 25% was most supported.

-

To avoid misalignment

between pay and performance, companies should be wary of paying executive

bonuses when severely impacted by COVID-19.

-

Large incentive payouts

lacking performance hurdles and the payment of bonuses where COVID-19 impacts

were severe, were the top two indicators of pay and performance misalignment

that would result in negative votes on “Say on Pay”.

-

With COVID-19, the

appropriateness of dividend payments when faced with liquidity problems, big

lay-offs, taking government subsidies and dilution of share capital were

ranked as concerns relatively equally.

-

A majority of survey

respondents support the adoption of loyalty shares.

D. Shareholder

Activism

-

Investors prefer to

influence boards by engaging with directors, followed by direct engagement

with management. Although ranking lower, collaboration with other investors

and voting against directors are also viable influencers.

-

After financial

performance, poor strategy, weak governance and misallocation of capital were

the highest-ranking reasons for supporting an activist.

-

Lack of responsiveness to

investor support for ESG resolutions and material ESG controversies could also

result in support for an activist.

-

A clear majority are

prepared to file or co-file an ESG-related resolution.

The complete

publication, including footnotes, is available here.

Endnotes

1

Global AUM = USD 110 trillion:

https://www.consulting.us/news/5332/asset-and-wealth-management-industry-to-grow-to-147-trillion-by-2025

(go back)

2

Morningstar, Global assets in sustainable funds hit record high of USD1.65trn: https://www.internationalinvestment.net/news/4026468/global-assets-sustainable-funds-hit-record-

usd-65trn-morningstar

(go back)

|

Harvard Law School Forum

on Corporate Governance

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2021 The President and

Fellows of Harvard College. |