THE

WALL STREET JOURNAL.

Business

Corporate Board Elections Getting a Little Less Cozy

This year, 478 nominees for U.S. board seats failed to win support

from a majority of voted shares, a 39% jump from 2015

|

BlackRock issued voting guidelines indicating that it expected

boards to have at least two female directors. PHOTO: LUCAS

JACKSON/REUTERS |

By

Theo Francis

Oct. 8, 2019 7:00 am ET

For decades, elections for corporate boards carried

little suspense. Most candidates ran unopposed and won by a landslide.

But board votes are no longer such a sure thing.

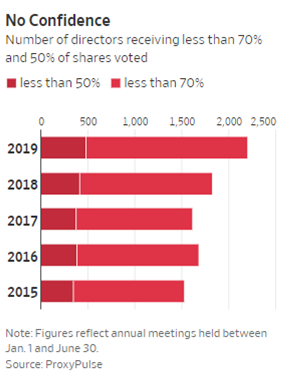

This year, 478 public-company directors failed to win the support

of a majority of voted shares, up 39% from 2015, according to a

new analysis

from

Broadridge Financial Solutions

Inc., which processes proxy votes for companies, and consulting firm

PricewaterhouseCoopers.

A total of 1,726 directors failed to

secure support from at least 70% of voted shares, according to the ProxyPulse

report, produced jointly by the two companies. The analysis covered about 4,000

U.S. companies holding annual meetings between Jan. 1 and June 30, the peak

period for board votes.

Despite the rise in rejections, only a fraction of directors were

snubbed by shareholders: There were 22,520 directors who stood for election

during this period in 2019. On average, directors won 95% of the vote, the study

found.

At some companies, boards can choose to retain directors that

fail to win majority support, but the practice is frowned on by investors.

Increasingly, investors have sought rules requiring directors to win a majority

of shares voted to retain their seats.

Most directors losing shareholder support aren’t at companies

involved in proxy battles—in which activist investors seek to replace board

members

with candidates of their own,

such as at

Procter & Gamble

Co. in late 2017 or at

Arconic

Inc. earlier

that year.

More typically, investors vote against incumbents without seeking to replace

them directly.

Among the 500 most widely held public companies—which are

generally also the biggest—50 directors failed to win a majority of shares voted

in 2019, compared with 15 recorded in 2015. The number of directors failing to

win at least 70% of the vote more than doubled to 170, from 69.

When directors lost shareholder support, it tended to reflect

lack of confidence from institutional investors rather than individual

shareholders, the analysis found. That is because small investors can more

easily sell their shares if they don’t like a company’s practices, said Chuck

Callan, Broadridge’s senior vice president for regulatory and corporate affairs.

“If they don’t like a stock, they’ll vote with their feet,” Mr.

Callan said. By contrast, many institutional investors have little choice but to

stay, in some cases because they manage index funds or other portfolios obliged

to hold stakes in certain industries or companies.

Investors appear most likely to withhold support for members of

board nominating and governance committees, said Paul DeNicola, principal of

PwC’s Governance Insights Center. That likely reflects the increased interest

among institutional investors in diversity and other board-composition issues.

In early 2018, for example,

BlackRock

Inc. —the world’s biggest asset manager—issued

voting guidelines

indicating that it expected boards to have at least two female directors.

Investors have avenues other than board votes to protest other

kinds of concerns. Investors unhappy with executive-pay practices, for example,

can vote down regular “say on pay” advisory votes over a company’s compensation

program, Mr. DeNicola said.

Write to

Theo Francis at

theo.francis@wsj.com