THE

WALL STREET JOURNAL.

Markets

Giant Investors Are Coming After One of Wall Street’s Cash Cows

Fidelity, T. Rowe, Wellington, others collaborating to meet

corporate CEOs without bank handlers

|

Fidelity Investments and other firms are planning a series of

private conferences where their analysts can meet CEOs. PHOTO:

GO NAKAMURA FOR THE WALL STREET JOURNAL |

By

Liz Hoffman and Geoffrey Rogow

June 26, 2019 9:33 am ET

Wall Street’s role as matchmaker between big money

managers and corporate executives is under threat.

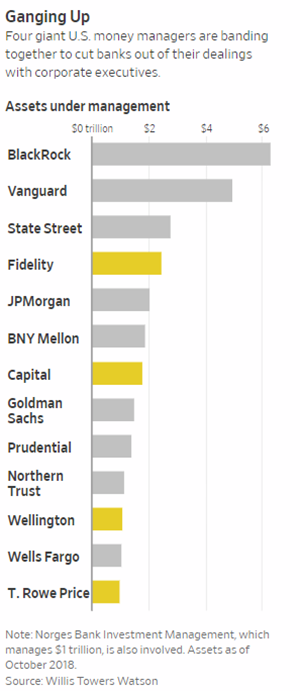

Next year, five large investing

firms overseeing more than $7 trillion are banding together to directly organize

a series of meetings with company executives, according to people familiar with

the matter. The first meeting, set for Boston next spring, will host executives

of consumer-staples companies.

The existence of the meetings is a

direct threat to the hundreds of millions of dollars in fees banks make each

year introducing their investor clients to the managers in whose companies they

own stock. Fund managers pack into hotel ballrooms to hear presentations and

take guided tours of company factories. A one-on-one meeting with a chief

executive can run $50,000 or more in some cases.

Now, some of the biggest managers

are planning to go it alone. No banks needed, or even invited.

Fidelity Investments, Capital Group,

Wellington Management, T.

Rowe Price Group Inc.

and Norway’s government fund are planning a series

of private conferences where their analysts can meet CEOs, according to people

familiar with the matter. The agenda: cocktails and dinner, followed by a full

day of one-on-one meetings, 75 minutes each. CEOs only.

“We plan to partner on corporate

access events and conferences that will provide a tailored research experience

for our investors,” a spokeswoman for T. Rowe said.

The workaround is just the latest

way that banks are losing their spots as Wall Street’s indispensable middlemen.

They once underwrote loans, stood in between buyers and sellers of securities,

and organized meetings between investors and corporate executives—all for hefty

fees.

Today, companies are increasingly borrowing

straight from loan funds, without hiring a bank to underwrite and

place the debt. Online platforms allow investors to trade directly with each

other, sidestepping a bank’s trader. Solo advisers help

companies design complex derivatives for a fraction of what Goldman

Sachs Group Inc. or JPMorgan

Chase & Co. would charge.

Corporate access is one of the few

cash cows left for banks and their research departments. Greenwich Associates

estimates that corporate access was worth $900 million to banks last year, about

12% of their total equities revenues. It can also spur trading revenue and draw

corporate clients closer.

The average big U.S. company sent

executives to six investor conferences and on five roadshows in 2017, where they

typically met with investors curated by a bank research department, according to

data provider IHS

Markit .

Chief executives get the chance to

tell their stories to sometimes skeptical audiences and soften up the ground for

shifts in direction. These meetings are generally unrecorded, with analysts

taking notes that they may later disseminate, in edited form, to other clients.

|

A

one-on-one meeting with a chief executive can run $50,000 or more in some

cases. |

Executives are forbidden from

sharing nonpublic information at closed meetings, but investors focus

on their body language and parse their words in the hopes of picking

up a useful nugget or two. A 2011 study found that fund managers who took

corporate meetings made more money than peers who didn’t.

The practice traces to 2003, when

Wall Street securities firms paid $1.4 billion to settle allegations that they

routinely issued overly optimistic stock research to flatter corporate clients

and win their investment-banking business. Regulators forced banks to wall-off

their research departments from their dealmakers.

So analysts turned to the access

business, finding another way to profit from their ties to big companies. In the

year following the settlement, at

least eight firms set up dedicated units to arrange intimate meetings

between investors and corporate brass. Some charged fees for entry; others

sought to curry favor with funds that might send more trades their way.

Banks have been relying more on that

business recently as trading commissions have dwindled and a shift to passive,

indexed investing has hit banks’ trading desks hard. The dense financial reports

their analysts produce are less relevant as computer-driven “quants” and index

funds displace traditional stock-pickers.

Consulting firm Oliver Wyman expects

banks to lose as much as $3 billion as asset managers cut back on research

spending. Charging for corporate meetings helps compensate. Investment banks are

now required by new regulation that began in Europe to tell their clients how

much they are charging them for research, rather than bundling its cost in with

trading commissions.

But their asset-manager clients are

similarly under pressure. The race toward low-fee funds pioneered by Vanguard

Group and BlackRock Inc.

two giants

notably absent from this latest effort—has forced rivals to slash costs, cut

jobs and even move their corporate headquarters to cheaper locations.

As ownership has become more

concentrated in the hands of a few asset managers, some investors question the

need to have banks in the middle at all. Just four firms—BlackRock, Vanguard,

Fidelity and State

Street Corp. —

were the largest shareholders in nearly 90% of the companies listed in the S&P

500 at the beginning of 2018, according to Brookings Institution.

The conference being organized by

the five firms could threaten popular conferences hosted by banks including Barclays PLC

and Bank

of America Corp. The

latter’s is historically held in March, around the time Fidelity, T. Rowe and

the others will gather in Boston.

Write to Liz

Hoffman at liz.hoffman@wsj.com and

Geoffrey Rogow at geoffrey.rogow@wsj.com