Educating Investors Through Leading

Questions

Posted by James McRitchie, CorpGov.net, on

Friday, May 17, 2019

|

Editor’s Note:

James McRitchie is the publisher of CorpGov.net. |

Bias in the world of

politics has spread to proxy voting controversies. A recent

paper by the Spectrem Group

purports to be “providing a voice to retail investors on the proxy

advisory industry” by employing a survey, which seeks to “educate”

respondents through leading questions. The report’s catchy title is

Exile of Main Street: Providing a Voice to Retail Investors on the

Proxy Advisory Industry.

Bias Feeds Off Itself

One technique used by the Spectrem Group is to quote previously

biased research.

|

Proxy Monitor

found that in 2017, “A limited group of shareholders has submitted the

overwhelming majority of shareholder proposals. Just three individuals and their

family members sponsored 25 percent of all proposals.” |

Although presented as representing the universe of proxy

proposals, the Proxy Monitor database contains only a select list of issuers. In

contrast Proxy

Insight‘s database follows proposals at all public companies in the

United States. A quick search of Proxy Insight’s database found that out of 611

proposals in 2017, the three individuals and their families mentioned by Proxy

Monitor (myself included) sponsored 110 or 18%, not 25%. Left out of Proxy

Monitor’s analysis is that those proposals averaged 38% support, compared to an

average 33% for proposals from all proponents.

Reliance on Character

Assassination

The Spectrem Group follows the above mentioned quote with the

following completely unsubstantiated allegation:

|

Thus, it would appear that a small number of conflicted parties

may be using low retail shareholder voting interest or participation to leverage

their influence in ways that run directly contrary to the preferences of those

shareholders. |

How are the three individual shareholders and their families

“conflicted” and how do their proposals “run directly contrary” with the

preferences of shareholders? Levels of support for our proposals is generally

higher than those presented by other groups, so do not “run directly contrary to

the preferences” of shareholders. The paper provides no evidence supporting its

allegations.

False Choices

The report contends that “91 percent of retail investors

indicated a preference for wealth maximization over political/social

objectives.” Investment objectives involve more than binary choices yet survey

respondents were asked to choose between “Fully pursue social/political

initiatives” and “Fully pursue maximizing returns.” Given that choice, what

person saving for retirement or education would choose to “fully pursue

social/political initiatives” with their investments?

Most people attempt to balance earning a good return with doing

no significant harm, although each person may have different values. For

example, one may choose to avoid investing in a company that makes a substantial

portion of its profits from slave labor because they find the practice

repugnant, while another avoids producers of cancer causing chemicals because

potential corporate liabilities might harm profits. We all have a multitude of

values and means of expressing them. Many want to earn money through their

investments, while also making the world a better place.

All investment funds I know of seek profits; I do not know of any

whose primary purpose is to support social or political initiatives.

Labeling is Not Educating

|

Upon completion of the survey, which included industry context, we not

only discovered that a large majority of investors support SEC oversight; we

found that more than three quarters of investors became more supportive of SEC

oversight. This highlights the critical roles of education and communication in

informing retail investors |

One example of such “education” is around the issue of using the

advice of an advisor with regard to proxy voting. The survey asked respondents

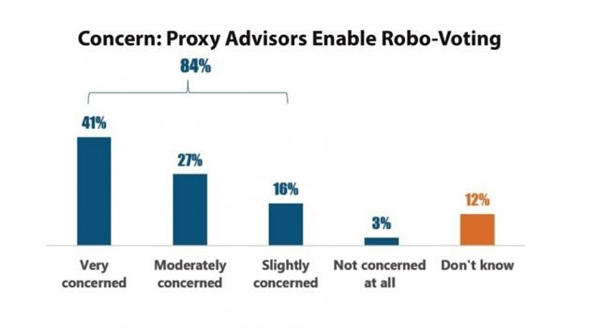

how informed they feel they are on proxy advisory firms. Only 6% felt they were

very informed. Here is where “education” came in. Those surveyed were asked

about “potential issues,” such as “robo-voting.” Only 5% responded they were

very familiar with “robo-voting” but when asked if they were “concerned” about

robo-voting, 41% answered they were “very concerned.”

Few respondents professed to know anything about “robo-voting.”

The survey then presented “robo-voting” as a “potential issue.” Robo-voting

sounds like robocalling

or votebots.

It is not surprising that 41% of respondents were “very concerned” and 27% were

“moderately concerned.” But the definition of robo-voting is never explained in

the survey, other than to label it a “potential issue.” Potential issues, by

definition are not good.

What is “robo-voting?” That is hard to tell. My guess is that it

is a term like zombie

proxy proposals that has been market tested by a group like the U.S.

Chamber of Commerce and found objectionable enough to drive public opinion.

Think “death tax” as a substitute term for estate tax.

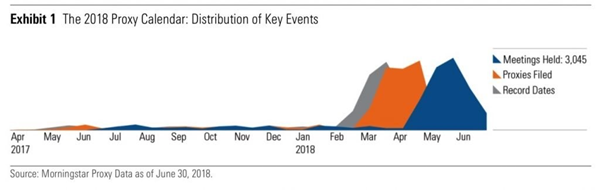

Institutional investors hire proxy advisors to help them research

issues and items that appear on corporate proxies, as well as to utilize their

voting platforms. Many funds have investments in thousands of companies. They

need to vote at hundreds of companies a day during the short proxy season. See

Exhibit 1 below from Morningstar.

Many proxy advisor clients provide their proxy advisor(s) with

proxy voting guidelines, which the advisor uses to pre-populate voting

instructions on the ballot. When ballots are ready for review, clients are

alerted. They can choose to restrict submission until specified client personnel

review and approve the votes or vote automatically, with the opportunity to

review and change votes until the voting deadline passes.

Voting results often mirror proxy advisory recommendations

because recommendations are based on input from clients and commonly accepted

governance principles. To call this “robo-voting,” driven by the power of proxy

advisors, demonstrates a lack of knowledge the process. If I tell you to vote in

favor of all proposals of a specific type, like declassifying the board, and you

comply, that is simply following my instructions and should not be considered

problematic like unwanted robocalling.

Although the Spectrem Group claims to measure “if retail

investors unaware of proxy advisory issues would change their level of support

for SEC oversight as they became more knowledgeable,” the report is a better

measure of market testing terms, such as “robo-voting” to sway public opinion. I

could go over the other four areas identified by the study as “potential

issues.” The result would be to highlight similar leading questions and what

appear to be opaque motives.

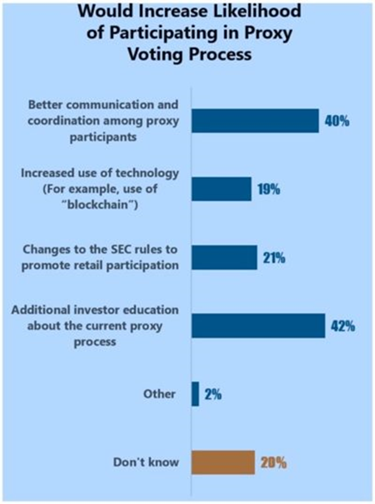

Redeeming Value

The report is not without redeeming value. There were a few less

leading questions aimed at driving retail shareholder participation. For

example, one question asked, “Which of the following would increase your

likelihood of participating in the proxy voting process?” Additional education

(42%) and better communication and coordination among proxy participants (40%)

would make investors more apt to participate.

[3]

Unmentioned by the report is that the SEC does little to inform

shareholders of their rights to file shareholder proposals or vote proxies. Most

of Investor.gov

is devoted to investors as consumers, not as owners. The focus is on protecting

investors against fraud. There is one

page on shareholder voting. The last update appears to have been in

2012. While the page discusses the mechanics of voting, it says little to

nothing about how to research proxy voting items.

Additionally, the survey found investors favored receiving more

information on how proxies are voted by asset managers on their behalf. Only 33%

of those surveyed indicated “Current vote disclosure from asset managers is

sufficient.” That may be the study’s most significant real finding.

[4]

Most of those surveyed by the Spectrem Group will never vote

proxies. They hold their “shares” through mutual funds and ETFs. Since 2003,

funds have reported their proxy votes but do so long after news coverage of

annual meetings has passed. Votes are filed with the SEC in a format that is not

sortable or user friendly.

If the Spectrem Group and J.W. Verret really want to empower

retail investors, they should advocate real-time proxy vote disclosure in a

sortable format. Those holding shares would then be more likely to vote because

of improved knowledge of how and why funds are voting as they do.

Additionally, fund investors would be able to move their money to

funds that vote in alignment with their own values. Many would try to invest

with funds that vote solely to “maximize shareholder value,” as J.W. Verret

Spectrem Group appear to advocate. Others would try to invest with funds that

vote for environmental, social and governance (ESG) improvements for better

long-term prospects. Why not let the market decide?

Providing more such information would make markets more efficient

and would put Mr. and Ms. 401(k) and Main Street investors in the drivers seat.

See my Draft

Petition to SEC for Real-time Proxy Vote Disclosure at SSRN or at CorpGov.net.

Compare the sortable disclosure of Trillium

Asset Management under the “Search Proxy Votes” tab, which even

includes the rationale for each vote, with that of the Vanguard

Index Trust Total Stock Market Index Fund, which makes it difficult

to determine voting trends.

The Spectrem Group’s next survey should ask if investors want to

see the proxy votes of their mutual funds and ETF’s before they are due or a

year or more after they are counted. Why not ask if investors want those records

in unsortable pdf format or in a sortable database to facilitate comparison? We

can guess how most investors would respond.

Endnotes

1

Spectrem

Group, “Exile of Main Street: Providing a Voice to Retail Investors on the Proxy

Advisory Industry,” 2019, graph on page 12. Available

here.

(go back)

2

Morningstar

Manager Research, “The Proxy Process: Raising the Investor Voice to Address New

Risks,” February 2019, page 3.

https://www.morningstar.com/lp/the-proxy-process?cid=CON_BLG0017

(go back)

3

Spectrem Group, “Exile of Main Street: Providing a Voice to Retail

Investors on the Proxy Advisory Industry,” 2019, graph on page 8.

Available

here.

(go back)

4 Spectrem Group, “Exile of Main

Street: Providing a Voice to Retail Investors on the Proxy Advisory Industry,”

2019, graph on page 8. Available

here.

(go back)

|

Harvard Law School Forum

on Corporate Governance and Financial Regulation

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2019 The President and

Fellows of Harvard College. |