THE

WALL STREET JOURNAL.

Markets

Mutual Fund Managers Try a New Role: Activist Investor

Portfolio managers increasingly are taking on corporate executives

with their demands for change

|

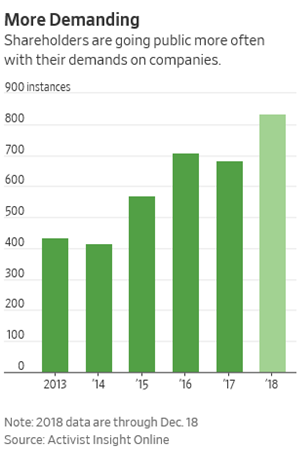

Investors like Neuberger went public with their demands 60 times

this year and in 79 instances in 2017 PHOTO: RICHARD B. LEVINE/NEWSCOM/ZUMA

PRESS |

By

Justin Baer and

Dawn Lim

Dec. 30, 2018 9:41 a.m. ET

Benjamin Nahum’s letters

to corporate executives don’t set off alarm bells like those from

billionaire investors like Carl Icahn or Dan Loeb.

Make no mistake, though, the Neuberger Berman Group LLC portfolio

manager is increasingly borrowing a page or two from their playbook: He’s

willing to scrap with the chief executives and board members of the small-cap

companies whose shares his firm owns.

“When you get into one bar fight and you win,” Mr. Nahum said,

“the next time you show up you get an even more serious audience.”

In the mutual-fund industry’s heyday, proxy fights and other

activist tactics were considered unseemly, and often pointless. If a manager

disapproved of managements’ actions, he or she would just sell the stock.

Today, they are taking on executives more frequently. Investors

like Neuberger went public with their demands 60 times this year and in 79

instances in 2017, according to data tracked by Activist Insight Online. There

were just 40 such public demands in 2014. Mr. Nahum launched one of Neuberger’s

first major public brawls about three years ago, criticizing pay at UltraTech

Inc. and calling for a shareholder vote that switched out some board directors.

These portfolio managers are also even more likely to push

quietly for changes. They are asking companies to alter the makeup of their

boards, run more environmentally friendly businesses or return more capital to

shareholders, investors say.

A more confrontational tone with management is just one of many

tactics active managers have tried to prove to their clients they’re worth their

higher fees. As billions of dollars continue leave stock pickers for low-cost

index funds, the industry finds itself in the fight for its future. To stem the

tide, active managers are turning to strategies ranging from novel

performance-fee funds to so-called alternatives such as private debt

investments.

Stock pickers aren’t the only ones taking on management. The

index-fund managers are trying to use their clout, too.

In his annual letter to fellow chief executives,

BlackRock Inc.’s Laurence Fink said his

firm would be more proactive. “The time has come for a new model of shareholder

engagement,” he wrote. Ten months earlier, fellow passive juggernaut State

Street Global Advisors launched a push to persuade companies to add more women

to their boards.

These index heavyweights’ approach

is different in several ways.

Active managers have teams of analysts who specialize in discrete

industries, and can identify specific weaknesses holding back a company’s

shares. Index investors instead prioritize a handful of issues and adhere to

codes on how to effect change over the long haul. Bound by the indexes’ makeup,

they can’t punish companies by dumping stock.

The large passive giants have also made a louder sales pitch.

“If Larry Fink is making statements saying companies have to

operate in a certain way and index funds are becoming more vocal, active

managers risk looking like the most passive money,” said Craig Wadler, a

managing director who advises companies on activist shareholders at investment

bank

Moelis & Co.

Even if they don’t succeed at enacting change from companies, the

index- fund managers succeed if they can erode a core reason clients were still

willing to pay higher fees for active firms.

“I see the quants, the passives, the activists, hedge funds and

private equity all raiding my client base,” said Mr. Nahum, who manages

Neuberger’s U.S. Small Cap Intrinsic Value Fund. “We’re under attack and losing

market share.”

Sweeping changes to the securities industry have altered the way

companies interact with their shareholders, said Jim Rossman, head of

shareholder advisory at

Lazard Ltd. Electronic trading and the

relentless concentration of stocks in the hands of fewer large shareholders

minimized Wall Street’s role as gatekeepers to the corporate world, he said.

There are now fewer active managers holding sizable stakes in

many companies. That’s made it harder for companies to freeze out those more

critical of management.

“It took some time, but many of these active owners woke up to

the fact that if they wanted to realize more value from their investments,

they’d have to become more active owners,” Mr. Rossman said.

Lucian Bebchuk, a Harvard Law School professor, said it is still

rare for a traditional manager to be openly critical of companies. “Like index

funds, most of the major mutual fund families that focus on active funds display

a deferential attitude toward corporate managers in their stewardship choices

and activities,” he said.

There can still be consequences for rocking the boat. Managers

don’t like to draw attention to investments that haven’t fared well, and that

can happen when they tell the outside world a stock they’ve held for years is

underpriced.

And while the Securities and Exchange Commission’s Regulation FD

rules ban companies from doling out information selectively, managers might

still get a cold shoulder from executives if they are too critical.

“You bear the mark of a troublemaker,” Mr. Nahum said. “You might

get shut out of small group meetings.”

Mr. Nahum said that happened to him earlier this year we he tried

to join an investor trip to software firm

Verint Systems Inc. Verint had appointed a

director proposed by Neuberger in early 2017. Mr. Nahum said he signed up for

the outing with the Wall Street firm that had arranged it; later, he was bumped;

the company wanted to give his spot to a newer investor. Verint officials did

reach out, and within two weeks Mr. Nahum said he had a one-on-one meeting with

the CEO.

A call to Verint’s investor-relations office wasn’t returned.

Write to

Justin Baer at

justin.baer@wsj.com and Dawn Lim at

dawn.lim@wsj.com