THE

WALL STREET JOURNAL.

BUSINESS

| JOURNAL

REPORTS: LEADERSHIP

Private-Equity Firms Rethink Their Short-Term Focus

Some look to stay

invested in companies for unlimited periods

|

Big investors like California

Public Employees’ Retirement System are helping drive the trend

to longer-term investments. Above, Calpers Chief Investment

Officer Ted Eliopoulos. PHOTO: RYAN ANGEL MEZA FOR THE WALL

STREET JOURNAL |

By

Dawn Lim and

Laura Cooper

June 19, 2018 10:27 p.m ET

Private-equity firms have

long hewed to a certain model: They raise investor money to buy

businesses, then exit their bets in a decade or so.

Now, some private-equity firms want

to stay invested in companies longer, perhaps even forever, driving a broad push

by the industry into longer-life pools, and what some call permanent-capital

funds.

BlackRock Inc., for

instance, is seeking more than $10 billion for a new private-equity pool that

has no deadline for exiting the investments it makes. Other companies, including

Altas Partners, Blackstone

Group,

CVC Capital Partners & Co. and Vista Equity Partners, collectively have raised

or are still looking to raise billions of dollars for pools designed to last

longer than the typical 10- to 12-year funds.

KKR has amassed $9.5 billion to hold

companies for the long term, and well beyond the life of traditional

private-equity funds. KKR is currently investing $8.5 billion of that capital,

which is the largest pool of its kind and is backed by $3 billion of the

private-equity firm’s own balance sheet. The firm raised the remainder from

institutions, with a large amount coming from sovereign-wealth funds and

insurance companies.

Fewer flubs

There are clear incentives to a

long-term strategy for both the firms and the investors. For one, firms that

keep investments private for longer can lower the risk of flubbed initial public

offerings. There is also appetite among some large investors—sovereign-wealth

funds in particular—for more investment strategies that match their own

long-term strategic horizons, which often extend for decades or longer.

To keep these long-term investors

satisfied, firms managing permanent-capital funds typically purchase businesses

with recurring revenue—examples could include a dental-services chain with

regular customers or a software company with licensing agreements—that can flow

back to the funds’ investors as fee income for decades.

‘Holy Grail’

One technology banker has called

permanent-capital funds the “Holy Grail for private-equity firms” because they

help the firms compete with corporate buyers, which can essentially hold the

companies that they purchase indefinitely. Private-equity funds, in contrast,

face pressure to sell companies or take them public after a few years.

The trend to long-term

private-equity investments could have repercussions in broader capital markets.

A proliferation of long-life funds could further shrink the U.S. public market

as more companies can readily tap the private markets for money and delay plans

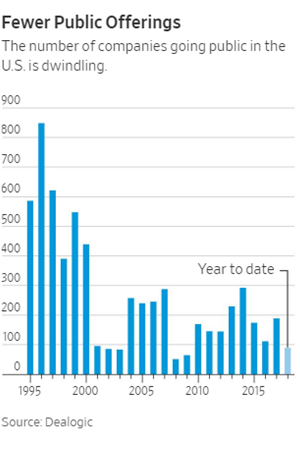

for initial public offerings. About 200 companies went public in the U.S. last

year, down from more than 800 in 1996, according to research firm Dealogic.

Another incentive of long-term deals

for private-equity firms is they may help the firms avoid the distraction of

having to market new funds every three or four years.

But the rise of funds built for the

very long run also raises the risk that private-equity managers become less

motivated to generate the outsize returns that have characterized the asset

class over the past decade or more. Indeed, it could become challenging for

firms to incentivize their deal makers to stick around when the investments they

make are expected to last for decades.

Too much

‘flipping’

The shift away from traditional

10-year funds shows large institutions are rethinking their relationships with

Wall Street.

“Investors with a long-term horizon

don’t see the point of investing in private-equity funds to hold companies for

just four or five years,” says Ludovic Phalippou, an associate professor of

finance at the University of Oxford’s Saïd Business School.

These investors want to avoid having

their managers become forced sellers of companies. Instead, they are warming up

to a view that institutions should back companies as long as possible to

maximize their profits.

Some big investors say they are

tired of finding themselves indirectly on both sides of a deal as private-equity

firms increasingly trade companies among themselves. The volume of such deals

globally rose to $93.7 billion in 2017, the highest level since 2007, according

to Dealogic.

“We’ve seen our own investments flip

four times through our portfolio from one manager to the next manager to the

next manager,” Jerry Albright, the investment chief of the Teacher Retirement

System of Texas, said at a pension meeting earlier this year. “In between those

flips, there’s fees.”

California Public Employees’

Retirement System, for its part, is exploring plans to set up

multibillion-dollar funds to buy and hold private companies for extended

periods. The idea would be to hold companies “forever rather than being forced

to sell them at an arbitrary time point,” Chief Investment Officer Ted

Eliopoulos told The Wall Street Journal in May.

Staying put

As it gets harder for investors to

find bargains when assets are increasingly overpriced, staying put in companies

may be more attractive than having to put cash to work.

For investors, one of the biggest

draws of a private-equity fund with an exceptionally long outlook is the lack of

more attractive investment options in a low-yield environment.

Institutions that have backed this

strategy “prefer to keep their capital invested for longer, rather than having

it returned quickly only to have to go out again to find opportunities to put it

to work,” says Webster Chua, KKR’s head of corporate development.

Ms. Cooper and Ms. Lim are Wall Street Journal reporters in New

York. Email them atlaura.cooper@wsj.com and dawn.lim@wsj.com.

Appeared in the June 20, 2018, print edition as

'Private-Equity Firms Think Longer Term.'