|

THE

WALL STREET JOURNAL.

Markets

Meet the New Corporate Power Brokers: Passive Investors

Index-fund managers such as Vanguard often cast deciding

shareholder votes on issues such as mergers and leadership changes

|

Michelle Edkins supervises how BlackRock, the world’s biggest

money manager, votes shares held in its passive funds.

PHOTO: JESSE WINTER FOR THE WALL STREET JOURNAL |

By

Sarah Krouse,

David Benoit

and

Tom McGinty

Oct. 24, 2016 10:41 a.m. ET

Investor Jeffrey Osher and his advisers arrived at the May annual

meeting of

Green Dot Corp., a prepaid-card

company,

thinking

they had enough votes to remove its chief executive from the board.

In

the parking lot, they discovered that was no longer true. Index-fund

giant Vanguard Group, the fourth-biggest shareholder, changed its vote

over the prior weekend to support the CEO.

The

reversal is a reminder of who now has leverage over America’s

corporate boards. It increasingly belongs to investors such as

Vanguard, pioneers of passive investment funds that track indexes

instead of trying to beat the market like Wall Street’s classic stock

pickers.

Passive funds

are increasingly the default investing

option for individuals and big pension funds alike. At the

end of June, U.S.-based mutual funds and exchange-traded funds that

track indexes owned 11.6% of the S&P 500, up from 4.6% a decade ago,

according to a Wall Street Journal analysis of data from

Morningstar Inc. and S&P Global

Market Intelligence.

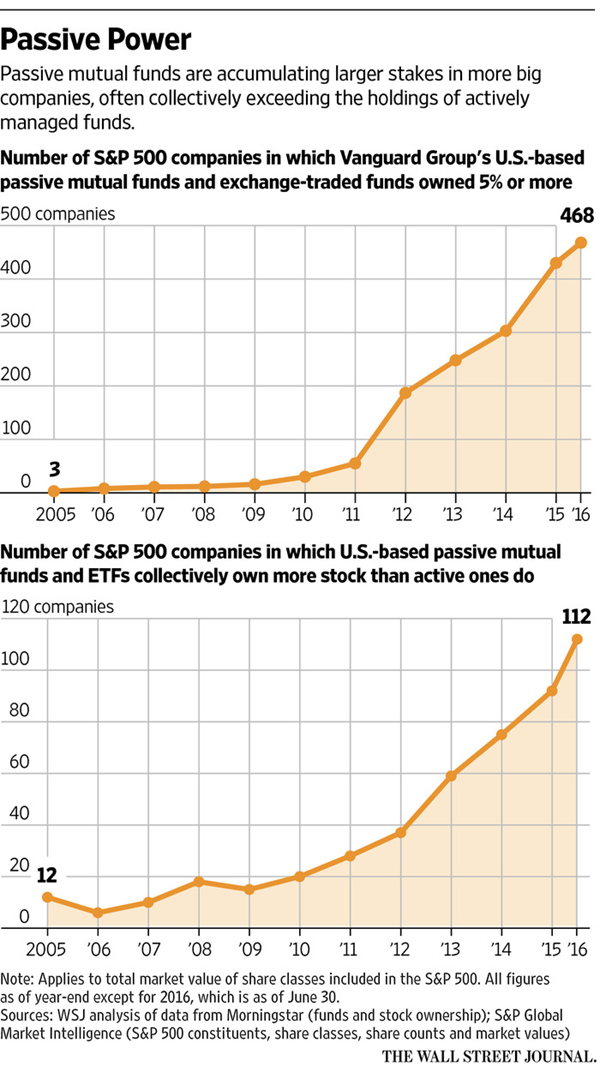

Vanguard’s U.S.-based passive funds owned 5% or more of only three S&P

500 companies at the end of 2005. By the end of June this year, that

number had rocketed to 468 companies, or about 94%, according to the

Journal analysis.

Passive funds used to be unequipped and unwilling to weigh in on most

corporate events. With their new power, they are waking up to how much

sway they can exercise over takeovers, the fates of chief executives

and other crucial decisions.

In June,

BlackRock Inc.,

another large passive investor,

voted against the executive pay plan at

Mylan

NV, which has since been embroiled in

controversy over its pricing of the EpiPen allergic-reaction drug.

BlackRock also cast an influential vote last year in favor of the $18

billion merger between professional-service providers

Towers

Watson

& Co. and Willis Group Holdings PLC.

Index-fund executives have added employees to deal with shareholder

votes, but say they don’t use their new power like activists

investors, who accumulate shares and make demands. They typically view

themselves as long-term holders that shouldn’t meddle in day-to-day

management.

“It’s not shareholders’ role to second guess what management is doing

in every single issue,” said Michelle Edkins, who supervises how

BlackRock, the world’s biggest money manager, votes shares held in its

passive funds.

The

change is shifting the clout in boardrooms toward investors known for

being deferential to management,

a stance troubling to stock pickers who

believe shareholders should assert themselves.

“As

more and more capital flows to index funds, the seriousness with which

these funds approach governance issues becomes even more critical for

U.S. and global corporate competitiveness,” activist

William Ackman wrote to his

hedge-fund investors earlier this year.

Daniel O’Keefe of investment firm Artisan Partners Ltd., an active

manager, contends that “the tyranny of passivity is you have large

pools of money that are unengaged in their investments,” which he

argues is “a far greater risk than the tyranny of activism.”

The last time such a concentrated group of owners had

as much control over U.S. companies as index funds do now was during

the era of

J.P. Morgan

and John D. Rockefeller, when those two businessmen had

board positions at a number of companies in which they were large

owners, researchers at the University of Amsterdam

wrote in a recent paper. They

eventually relinquished some of their power because of government and

public pressure.

In

the ensuing decades, stock ownership spread among individual

investors, leaving corporate managers largely free of powerful

stockholders with the ability to reshape their companies, the paper

said. It wasn’t until the rise of mutual funds in the 1990s that

single entities amassed large positions across so many companies.

When Vanguard started indexing in the late 1970s, founder John Bogle

gave the job of overseeing shareholder votes to one person, a staff

assistant. For years, Vanguard index funds voted some of their shares,

but didn’t devote significant resources to meeting with the management

of companies they held.

That has now changed. “We moved from a position of reluctance to make

our weight felt to absolute interest in making our weight felt,” said

Mr. Bogle, now retired from the firm.

Vanguard has 15 people overseeing work on about 13,000 companies based

around the world. BlackRock has about two dozen people who work on

governance issues at some 14,000 companies held in its index funds and

exchange-traded funds, and it plans to add seven more in the coming

months, according to a spokesman.

Boston-based

State Street

Global Advisors, another large passive-fund manager,

part of State Street Corp., has fewer than 10 employees devoted to

issues at around 9,000 companies and uses a number of automated

filters to identify companies on which to focus each year.

Mr.

Ackman, the activist investor, visited Vanguard in the summer of 2015.

It was several weeks after Vanguard, BlackRock and State Street had

backed

DuPont Co. management in a

shareholder vote, helping the chemical company defeat a campaign by

activist investor

Nelson Peltz and the firm he

co-founded, Trian Fund Management LP, to secure board seats. That vote

spurred concern among several activists that passive funds were simply

too passive.

Mr.

Ackman and Vanguard board members and executives presented different

views on what type of shareholder behavior leads to corporate change.

Mr. Ackman’s Pershing Square Capital Management LP has an investment team

of eight, plus Mr. Ackman and various other employees, for a portfolio

that normally includes about a dozen stocks.

Glenn Booraem, a principal at Vanguard who works on its governance

efforts, said in an interview that his team can’t effectively meet

with all the companies in Vanguard’s funds in one year. He said he

tries to take a longer view, communicating regularly with portfolio

companies in person, over the phone or via email.

Rakhi Kumar, head of corporate governance at State Street’s

asset-management unit, said she tells her team not to agree to every

meeting companies ask for because of time constraints. “If I don’t

have something to say to you, it’s meaningless,” she said.

Index funds say they

do watch over management. Their

executives say they have different investment time horizons and fee

structures than activists, which affects their decisions about

portfolio companies.

Before the vote at prepaid-card company Green Dot, Vanguard talked

with board members after the activist investor, Mr. Osher, argued the

company’s CEO and founder, Steven Streit, had to go, citing stock

declines and its disappointing earnings.

|

BlackRock has the world’s largest exchange-traded-fund business.

PHOTO: JESSE WINTER FOR THE WALL STREET JOURNAL |

Green Dot looked to persuade investors it was committed to change

while supporting its CEO. During the weekend before the shareholder

vote, it announced the resignation of two other board members.

That move was spurred in part by the discussions with Vanguard,

according to people familiar with the events.

Vanguard then voted for Mr. Streit, while

many active managers voted for the activist.

Index funds say they routinely talk to companies and use data and

research to make sure their approach to governance questions is best

for their investments and all shareholders over the long haul.

“We’re riding in a car we can’t get out of,” said Vanguard’s Mr.

Booraem. “Governance is the seat belt and air bag.”

A

study published in February by researchers at Boston College,

Washington University in St. Louis and University of Pennsylvania’s

Wharton School found evidence that higher ownership by passive

investors leads companies to

shed tactics seen as defensive against

shareholders, such as staggered-elected boards, and to

increase the independence of board members. It found little impact on

executive compensation or capital allocation, the kinds of operational

changes activists often seek.

How

BlackRock and the other big passive holders vote often determines the

outcome. Between 2014 and 2015, there were nearly 20 unsuccessful

shareholder proposals on environmental and social issues that would

have passed had BlackRock, Vanguard or State Street supported them,

according to a Journal analysis of data from Proxy Insight.

At

BlackRock, Ms. Edkins said she believes her team can have influence in

about 1,200 of the U.S. companies owned by its passive funds because

of the size of BlackRock’s stake or the company’s structure. She said

meetings behind closed doors can go further than votes against

management, and that BlackRock typically gives companies a year to

change before casting a dissenting vote.

BlackRock controlled 6.5% of drugmaker Mylan at the end of June,

making it the third-biggest shareholder. In meetings with the company

a few years ago, BlackRock raised concerns about executive

compensation and the company’s leadership structure, according to two

people familiar with the discussions.

Dissatisfied with changes that followed, BlackRock voted against the

company’s executive pay and the directors on the compensation

committee at the annual meeting this year, filings show. Mylan has

said its shareholders approved its executive-compensation packages. It

has since

come under fire for price increases on its

EpiPen, which in turn has drawn attention to its executive

compensation.

BlackRock’s was a sought-after vote in last year’s proposed $18

billion merger between professional-service providers Towers Watson

and Willis Group. Towers Watson investors were upset about the

proposed terms, a package of cash and shares in the combined company

worth less than Towers’s stock price when the deal was announced.

Proxy advisers Institutional Shareholder Services Inc. and Glass,

Lewis & Co. both

recommended voting against it.

BlackRock’s passive team leaned toward voting no, but portfolio

managers at the firm’s actively managed funds backed the deal, arguing

that it would create more long-term value, said people familiar with

the matter. The active managers persuaded their colleagues to do the

same.

Vanguard’s founder, Mr. Bogle, recalled unsuccessfully trying to rally

other index-fund managers in the early 2000s to form a group of

shareholders. At the time, one firm said index funds should leave the

performance of companies in their portfolios to “the invisible hand of

the marketplace,” he said.

These days, Mr. Bogle said, “we are the invisible hand of the

marketplace.”

—Coulter Jones contributed to this article.

Write to

Sarah Krouse at

sarah.krouse@wsj.com, David

Benoit at

david.benoit@wsj.com and Tom

McGinty at

tom.mcginty@wsj.com

|