|

THE

WALL STREET JOURNAL.

Markets

Oil Companies Are Still Paying Their CEOs to Pump

Many big production firms still base executives’ bonuses largely

on how much crude they find and extract

|

Chesapeake Energy CEO Doug Lawler received $1.56 million last

year for exceeding production and reserve targets, more than

half his total bonus of $2.69 million. PHOTO: BRETT DEERING

FOR THE WALL STREET JOURNAL |

By

Ryan Dezember

Updated May 16, 2016 11:11

a.m. ET

If investors hoped the

biggest oil bust in decades would change the way oil industry

executives are getting paid, they are probably disappointed.

Many large production

companies last year continued to incentivize their executives based,

in large part, on how much crude they found and extracted, according

to a Wall Street Journal review of filings from the largest U.S.

energy producers.

Executives received

sizable cash bonuses for finding and producing more oil and gas than

the year before, even though plummeting commodity prices made it

unprofitable to keep drilling many wells.

At

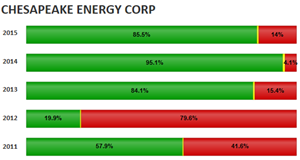

Chesapeake Energy

Corp., one of the country’s largest producers, Chief Executive Doug

Lawler received $1.56 million last year for exceeding production and

reserve targets, securities filings show. That was more than half his

total bonus of $2.69 million, according to the filings.

Chesapeake’s production

rose 4.9% last year, more than twice its 2% target. But its earnings

plummeted, and its stock lost 77%.

A Chesapeake spokesman

declined to comment.

“There needs to be a more

returns-focused element in this industry,” said Paul Grigel, a

Macquarie Group Ltd. senior analyst who tracks pay-policy changes

among energy producers. “This is an issue for a lot of longer-term

investors; it’s something they’re becoming very impassioned about.”

Mr. Grigel found that 14

of the 25 companies he studied either made no change in 2015, or

didn’t disclose the details of their bonus calculations. Four

companies increased their emphasis on production and reserve growth

last year, while seven lessened the importance of these factors.

Exploration and production

companies in recent proxy filings have disclosed their formulas that

determined last year’s cash bonuses. These will be followed by annual

meetings, where shareholders will have a say on pay practices.

Some corporate-governance

observers warn that investors won’t tolerate big bonuses based on

increased production if earnings and share prices are down.

“Many shareholders hope

that [bonuses] reflect the pain that investors are feeling in their

portfolio values,” said John Roe, managing director at ISS Corporate

Solutions, a unit of investment adviser Institutional Shareholder

Services Inc.

Incentive pay in the oil

patch helps explain why U.S. producers have been slow to dial down

their output despite a global glut of crude and domestic natural-gas

oversupply.

U.S. oil production has

declined about 7% since peaking at a four-decade high of about 9.7

million barrels last year. Natural-gas output, meanwhile, has remained

on an upward trajectory despite a yearslong price slump.

Rewarding executives for

growth at any cost is rooted in Wall Street’s treatment of exploration

and production shares as growth stocks. Since the advent of shale

drilling more than a decade ago, analysts and investors tended to

favor future prospects over profitability.

The collapse in commodity

prices has put that practice into question, though, as many companies

struggle under debt they piled up acquiring land and drilling. Yet

producers are hesitant to stop incentivizing growth all together.

These companies’ borrowing abilities hinge on how much oil and gas

they have discovered but not yet extracted and sold. If they don’t

replace enough of the volumes they sell each year with new

discoveries, they risk losing funding.

Overall, bonuses, which

usually account for less than a third of total compensation, broadly

declined last year because low commodity prices crimped profits and

sent stock prices tumbling.

Continental Resources Inc.,

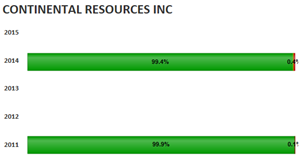

which drills in North Dakota and

Oklahoma, reduced the weight given to production and reserve growth in

its bonus math from 75% in 2014 to 34% last year, replacing its

incentives to simply find more oil and gas with one aimed at keeping

down the cost of doing so. Continental didn’t respond to requests for

comment.

Approach Resources Inc.,

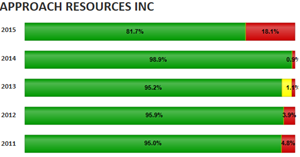

which idled rigs on its West Texas

drilling land last year in response to low oil prices, eliminated

reserve and production targets. It increased the importance of capital

efficiency and debt relative to profits. In 2014, production and

reserve goals accounted for a quarter of possible bonuses.

“We made the decision,

given commodity prices, that what was more important was achieving

attractive rates of return with shareholder capital, preserving

balance-sheet liquidity and living within cash flow,” said Sergei

Krylov, Approach’s finance chief.

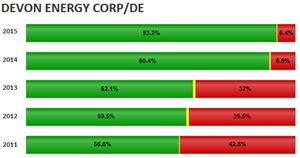

Devon Energy Corp.

in its proxy filing urged shareholders to

reject a shareholder proposal to eliminate reserve growth metrics from

its bonus formula. “Exploring for and developing undiscovered oil and

natural-gas reserves is fundamental to the company’s business and

critical to its ability to build and sustain value,” Devon said.

The Oklahoma City company

made production and reserve growth each worth 15% of possible bonuses,

up from 10% and 5%, respectively, in 2014. Though Devon exceeded its

production target, low commodity prices prompted the company to write

down the value of its drilling fields by $19.2 billion last year as

many of its drilling properties became uneconomical. That led to a net

reduction of reserves.

Missing its goal of adding

the equivalent of 140.4 million barrels of oil to its reserves cost

CEO David Hager more than $200,000, Devon’s proxy shows. Mr. Hager’s

2015 bonus was $1.55 million, about half what his predecessor earned

the year before.

Write to

Ryan Dezember at

ryan.dezember@wsj.com

|