|

THE

WALL STREET JOURNAL.

Business

Mutual Funds Flail at Valuing Hot Startups Like Uber

Prices for hot private companies are hard to set and can vary

widely; a 99% plunge at T. Rowe Price

|

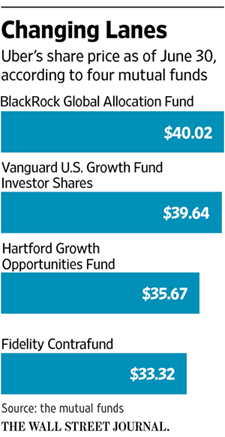

Mutual-fund managers at Fidelity Investments valued Uber's

shares at $33.32 apiece in June, but Vanguard Group said they

were worth $39.64. Above, the car-hailing company’s headquarters

in San Francisco. PHOTO: ERIC RISBERG/ASSOCIATED PRESS |

By

Kirsten Grind

Oct. 29, 2015 11:00 p.m. ET

Millions of Americans own a piece of the hottest private technology

companies through their mutual funds. But no one knows what those

investments are actually worth.

Consider car-hailing king Uber Technologies Inc., the world’s most

highly valued startup. As of June 30, mutual-fund managers at

BlackRock Inc. valued the firm’s stake in Uber at $40.02 a share.

Hartford Financial Services Group Inc. said $35.67. Fidelity

Investments said $33.32.

The differences are a sign of growing danger for individual investors

as mutual funds scramble to buy shares in new tech companies before

they go public. While

getting in early gives those mutual funds a shot at a huge profit

if a company takes off, which happened with

Facebook Inc. and

LinkedIn Corp., many funds struggle just to put a value on their

private-company shares.

In the stock market, prices rise and fall every day in response to

company announcements, economic news and jostling by droves of

investors. Private companies rarely talk in detail or disclose

financial information, leaving their investors in the dark and on

their own to decide how much a stock is worth.

Varying valuations

An analysis by The Wall Street Journal of closely held technology

startups worth at least $1 billion found 12 instances where the same

company was valued differently by more than one mutual-fund manager on

the same date.

The analysis was based on data from research firm

Morningstar

Inc. on about 90 venture-capital-backed companies tracked by the

Journal and Dow Jones VentureSource in a project called

“The Billion Dollar

Startup Club.”

The 12 companies with different prices at different mutual funds

included Uber, valued

at close to $51

billion in a funding round completed in July, and Dropbox

Inc., which was

last valued at $10

billion. The share-price gap ranged from a few cents per

share to more than twice the stock’s price.

Few mutual-fund firms are willing to discuss their valuation

procedures in detail, largely because of competitive concerns, but

mutual-fund firms say they follow a rigorous process.

Donna Anderson, who manages global corporate governance for

T. Rowe Price Group

Inc., says it sometimes feels like “being on a teeter-totter” while

the mutual-fund firm is carefully trying to determine the right price.

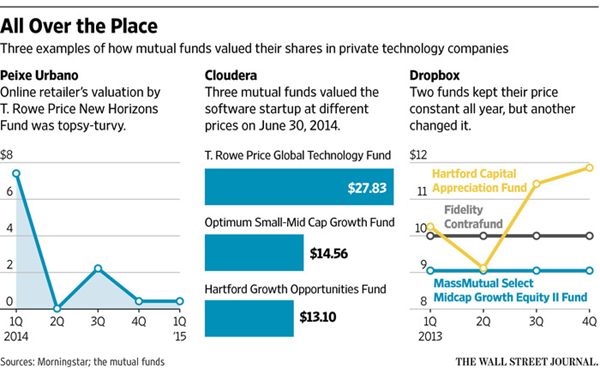

T. Rowe Price valued the stake held in software startup Cloudera Inc.

by the T. Rowe Price Global Technology Fund at $27.83 per share on

June 30, 2014. That was roughly twice as high as the valuation by

Hartford and

Macquarie Group

Ltd.’s Delaware Investments on the same day.

Big gaps like that suggest “you’re kind of getting a guess from the

fund company,” says Katie Reichart, a senior analyst at Morningstar.

Mutual-fund valuations of private companies are “pretty opaque,” she

adds.

The consequences can be dramatic. In last year’s second quarter, T.

Rowe Price slashed its valuation of Peixe Urbano from $7.41 a share to

three cents after concluding that the Brazilian online discount

retailer was likely to be liquidated.

Instead, Peixe Urbano was acquired by Chinese online search giant

Baidu Inc.

T. Rowe Price and other mutual-fund firms flip-flopped,

increasing their valuation on Peixe Urbano to $2.22 a share.

Private

Risk

Read a series exploring the intersection of Silicon Valley and

Wall Street in the technology boom.

|

|

For individual investors, the risks are mushrooming as mutual funds

buy more startup stocks than ever. Such stocks are highly appealing to

managers whose investment returns have been hurt by abnormally low

interest rates and this year’s lackluster stock market. Many of those

managers also are struggling to compete with lower-cost mutual funds

that track a market index.

Five of the biggest fund firms participated in funding rounds worth a

combined $6.1 billion at startup companies last year, up from about $1

billion in 2011, according to data from CB Insights. This year’s total

was $8.3 billion as of Sept. 30.

Mutual-fund firms typically get their shares in private companies when

they participate in funding rounds that are open just to a select

group of investors.

Regulators require mutual funds to limit their holdings of “illiquid”

securities to no more than 15% of a fund’s assets. Most mutual funds

have no more than a tiny percentage of their portfolio in startup

stocks.

Financial adviser Tim Parker says some of his clients have investments

in Fidelity Contrafund. He realized only recently that the giant fund

has exposure to Uber. Mr. Parker says he isn’t sure how the fund’s

managers decide what Uber shares are worth.

Fidelity Contrafund owned $162.2 million of Uber as of June 30 and has

total assets of about $103.4 billion. The mutual fund has made a paper

profit of $86.7 million, more than doubling its money since buying

Uber shares in June 2014.

“I would hope that they’re not jacking up the price to prices they

hope to get one day that are completely unattached to recent history,”

says Mr. Parker, a partner at Regency Wealth Management in Ramsey,

N.J.

A Fidelity spokesman says in a statement that the firm has “a rigorous

and thorough fair market valuation process for mutual fund holdings.”

Sean McKee, who audits mutual-fund firms’s private-company valuations

for KPMG LLP, says it is impossible for any investor to know how much

a company is worth until it goes public.

“Until you get to a point where there’s an IPO, there is no one

price,” Mr. McKee says.

Like all mutual-fund managers, those with shares of private technology

companies in their portfolio must assign a current value to the

securities every day so investors get a clear picture of how much the

holdings are worth. Changes can affect the fund’s overall net asset

value, or price per share.

But the shortage of information about private technology companies and

their tiny trading volume create daunting valuation hurdles for fund

managers.

At Fidelity, securities prices are valued in “good faith” when

officials are trying to gauge the impact of events outside the

markets, according to securities filings by the firm.

Mutual funds must disclose their holdings every quarter, though some

funds do so more often. To see how much a private company’s stock has

gone up or down, individual investors usually must do the calculation

on their own by comparing different securities filings.

Some experts say the rising popularity of private tech stocks is

hazardous simply because the shares are hard to sell, lack a broad

secondary market and could react wildly if the overall market swoons.

“We’re all waiting to see how that plays out,” says Babak Yaghmaie, a

partner at law firm Cooley LLP who represents young private and public

companies, including technology startups.

Ms. Anderson of T. Rowe Price says mutual funds are in a tough spot

because they all get different information from startups. “Sometimes

the randomness you’re seeing [with pricing] is we all see different

things,” she says.

At some funds, though, private technology companies are one of the

biggest single investments. Hartford Growth Opportunities Fund, run by

Michael T. Carmen, one of the best-known mutual-fund investors in

startups, had 1.7% of its $4.7 billion of assets in Uber at the end of

September.

In comparison, about 3.5% of the fund’s assets were in

Apple

Inc., which has a stock-market value of more than $650 billion. A

Hartford spokeswoman declined to comment.

Uber’s steep rise in value among investors who have pumped money into

the San Francisco company has bumped mutual-fund returns higher.

Andrew J. Shilling, a portfolio manager at Wellington Management Co.,

which oversees some of the assets in the Vanguard U.S. Growth Fund,

cited Uber as a

reason why the fund trounced its rivals in the latest

fiscal year.

|

Pure Storage CEO Scott Dietzen, right, and other company

officials ring the opening bell at the New York Stock Exchange

on Oct. 7 to celebrate the company's IPO. Last year, different

mutual funds valued the company's shares at far different prices

on the same date.

Photo: Brendan McDermid/Reuters

|

|

Securities filings show that Vanguard U.S. Growth Fund owns 1.4

million shares of Uber. The fund boosted its estimate of the stake’s

market value by 19% to $55.8 million between Feb. 28 and June 30.

Glenn Booraem, who handles Vanguard Group’s private-securities

valuation, says startups are “inherently more difficult to value on a

stand-alone basis.” That’s one reason why the firm’s portfolio

managers buy private shares “on a relatively limited basis,” he says.

A BlackRock spokesman said in a statement that the firm’s valuation

team “has a rigorous and robust process for valuing private holdings

and regularly updates valuations based on multiple sources of

information.” An Uber spokeswoman declined to comment.

There are no regulatory guidelines for mutual-fund firms to follow,

other than to not knowingly misprice securities.

In 2004, Van Wagoner Funds, a large investor in privately held

startups during the tech-stock boom of the 1990s,

settled civil charges

in which the Securities and Exchange Commission alleged that the firm

misled shareholders about the size and value of the funds’ investments

in illiquid securities.

The mutual-fund firm and its president, Garrett Van Wagoner, agreed to

pay an $800,000 penalty without admitting or denying the allegations.

Mr. Van Wagoner says the firm closely followed its valuation policies

and procedures. “We thought deep and hard about what was the true

value of these securities, but we found out the fundamentals of the

companies were going into a nuclear winter, so we aggressively wrote

them down,” he says.

An SEC spokesman declined to comment on whether agency officials have

any concerns about the valuation procedures now used by mutual funds.

‘Exhaustive’ process

Some mutual funds say it is so hard to value startups from day to day

that they limit their investments in those companies or avoid them

entirely.

Aram Green, a managing director and portfolio manager at ClearBridge

Investments, has invested in just one startup this year, partly

because of what he calls an “exhaustive” valuation process after

buying such stocks.

“I underestimated how time-consuming the process is,” he says. It

includes frequent meetings by the valuation committee of ClearBridge’s

parent,

Legg Mason

Inc.,

to decide if a stock’s price should be changed.

“It’s a lot of information and analysis on a real-time basis,” Mr.

Green says.

Some fund managers turn to private companies for information that

could affect the stock price. But different managers often get

different levels of detail from the same company depending on terms of

their investment, including the type of shares bought by the mutual

fund.

In return, some mutual-fund managers get “board observation rights,”

which allow them to listen to a company’s board meetings.

Lower-ranking investors might get just a copy of the company’s

unaudited financial statements every quarter, according to accountants

and fund executives.

Sometimes, mutual funds don’t change their price of a startup’s shares

for a year or more. Fund executives say that reflects the information

shortage.

In 2013, Fidelity Contrafund never changed its quarterly price on

Dropbox, according to data from Morningstar. Neither did the

MassMutual Select Midcap Growth Equity II Fund, though the two funds’

per-share valuations of Dropbox were about 10% apart.

In contrast, Hartford Capital Appreciation Fund moved its valuation of

Dropbox up or down in all four quarters of 2013. The three funds

sharply boosted their valuations after the online storage provider

completed a new funding round.

Fidelity, Hartford and Dropbox declined to comment. A spokesman for

the MassMutual mutual fund, part of insurer Massachusetts Mutual Life

Insurance Co. couldn’t be reached.

In March 2014, Fidelity’s flagship Fidelity Magellan Fund valued

storage systems maker

Pure Storage

Inc.

at $9.25 a share. T. Rowe Price New Horizons Fund said

Pure Storage was worth $6.93 a share—or 25% less.

Pure Storage completed a funding round in April 2014. In June, the two

mutual funds valued the company at $15.73 a share. The company

went public in

October at $17 and now trades near $18.

Fidelity and T. Rowe Price wouldn’t comment on the values they

assigned to Pure Storage shares.

The swings in Peixe Urbano’s valuation show how hard it is to piece

together an accurate picture of a startup company. T. Rowe Price

bought its stake when daily deals sites like

Groupon

Inc.

and LivingSocial Inc. were popular.

But by mid-2014, “it was very clear” that Peixe Urbano was “not on

plan,” says Ms. Anderson of T. Rowe Price.

The firm says it has a rigorous, longtime valuation process that

examines many factors related to startups.

The firm’s New Horizons Fund owned about 600,000 shares of Peixe

Urbano. Morningstar says the 99% slide probably didn’t affect the

fund’s overall performance last year because Peixe Urbano was less

than 0.5% of the fund’s assets. A Peixe Urbano spokeswoman declined to

comment.

T. Rowe Price was taken aback again when Baidu swooped in to rescue

Peixe Urbano by buying a controlling stake.

It was “a surprise move, at least to us,” Ms. Anderson says.

Write to

Kirsten Grind at

kirsten.grind@wsj.com

|