Finance

Activist

Investors

Actively mediocre

by Anne

VanderMey

April 21, 2015, 9:18 AM EDT

|

|

Courtesy of Jeff Sonnenfeld

|

Activist investors scold CEOs over stock

prices, but their own returns are just so-so.

There’s no question that activist investors are ascendant.

Increasingly a force in even the most elite boardrooms, these

shareholder standard-bearers agitate for change, aiming to boost the

profit and stocks of their target companies. And most often, they’re

hedge fund managers who, in the process, charge their clients gaudy

fees (typically 2% per year plus 20% of any gains).

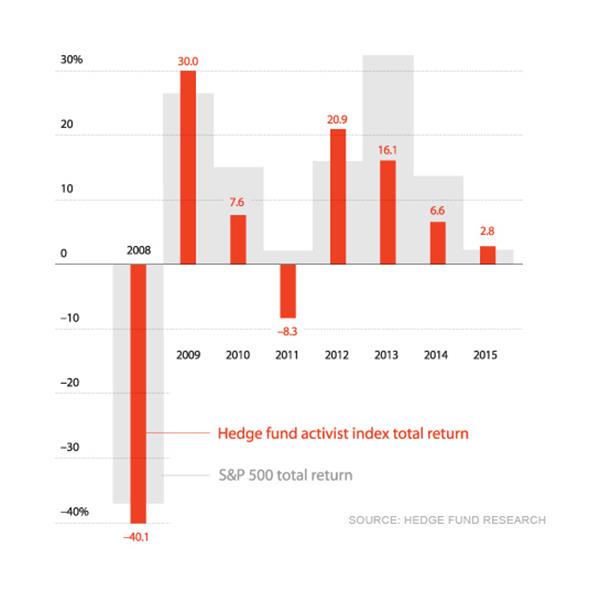

But how are the returns of the activists’ own funds? Taken as a whole

over the past seven years … not all that great.

According to data compiled by research firm HFR, activists beat the

S&P only three years out of the past eight, including by a narrow

margin so far in 2015. “They can dish it out, but they can’t take it,”

says Yale School of Management professor Jeffrey Sonnenfeld, who for

years has been sounding the alarm about funds he thinks squeeze

companies for short-term gains. If you invested in the average

activist hedge fund at the start of 2008, your cumulative return today

would be 19% after fees, according to HFR; for the S&P 500, with

dividends, it would be 65%.

Hedge fund defenders say it’s unfair to look at such a short time

frame (2008 was the first year HFR tracked activist performance on its

own). Plus, HFR’s index looks at a universe of more than 70 firms, not

all of them stars. The average obscures performances like that of

Sonnenfeld critic Nelson Peltz, who says the flagship fund of his

Trian Fund Management has notched a 137% return after fees since its

2005 inception. (The comparable figure for the S&P would be just over

100%.)

Should CEOs follow the activists? That’s a tricky call. For average

investors (most of whom couldn’t get access anyway), the answer is a

lot easier: Stick with an index fund.

This story is from the May 1, 2015 issue of Fortune magazine.. |