|

Focus

Group: Is patience a virtue?

November 2014 (Magazine) | By

Dominic Gane

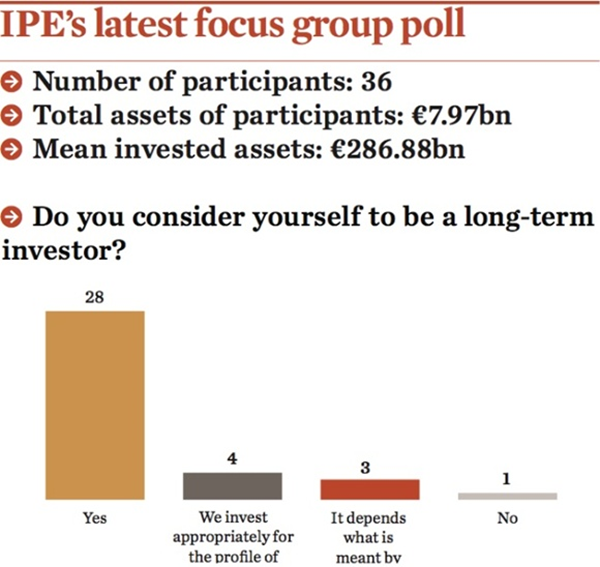

Over three-quarters of respondents polled for this month’s Focus Group

consider their fund to be a long-term investor.

But

the devil is in the detail. For one UK fund, long-term investing means

“engaging with the companies in which we invest to ensure that they

are taking decisions that protect their long-term earnings potential”.

Many relate their investment horizon to the duration of their

liabilities, which may or may not have a long horizon. One contrasts a

long-term “strategic orientation” with the variety of time horizons

taken across asset classes.

For

three respondents, it depends on what is meant by ‘long term’. “If

long term in your sense means more ‘illiquid’, then we’d disagree,”

said a UK corporate fund. “We prefer liquid investments which generate

income and income growth and liquid markets which offer us the

opportunity to recycle capital by realising intrinsic (fair) values

and reinvesting opportunistically.”

When

asked to pin down their assumptions, a quarter defined long-term

investing in public markets as taking a three to five-year view. A

third saw it as a seven to 10-year view. Only six were prepared to

take a “generational view” of 15 years or more. “A decade is a period

of time we consider as suitable to define long term,” said an Austrian

fund. “On one hand, not many investments have a longer lifetime and,

on the other, it matches with the liabilities based on our business

model.”

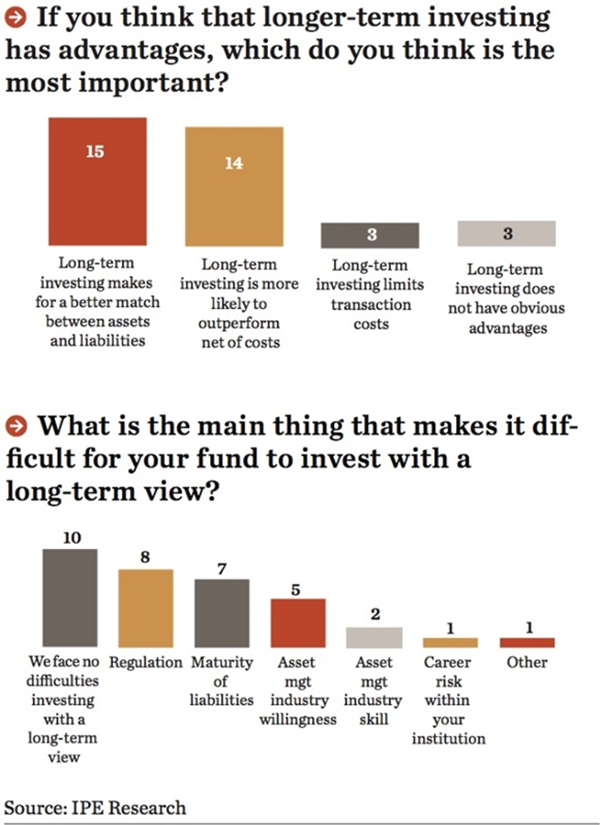

Fifteen respondents think the best advantage of long-term investing is

that it makes for a better match between assets and liabilities, while

14 think it is more likely to outperform, net of costs. Three

respondents think it has no advantage.

Ten

respondents said that they face no difficulties investing with a

long-term view. For the rest, regulation is considered the main

difficulty. A UK local government fund was candid: “Our investment

regulations are 20 years out of date. We have been promised a full

re-write for five years-plus, but the Department for Communities and

Local Government (CLG) has just tinkered. Rather than waste time with

consultations on active versus passive, CLG should address this.”

The

willingness of the asset management industry to meet the needs of

long-term investors was also cited as a problem. Sixteen funds have no

problem finding public-market asset managers that are willing and able

to invest for them long-term. A further seven find it more difficult,

with a Swedish fund highlighting that the “incentives of managers are

not always the same as ours”. One UK local authority fund said:

“Active managers seem to think that their title means that they have

to trade.”

Nine

can only find managers for certain classes or strategies. A UK fund

contrasted long-term investments in illiquid private markets with

public markets that are “driven by short-term liquidity and

mark-to-market ideology, which is anathema to long-term investing,

which is about long-term sustainable cash flows”.

Three-quarters of those polled feel their fund has genuine

transparency into all the fees, charges and expenses it incurs through

active portfolio management. Eight funds feel the opposite; a UK fund

said “fund of funds arrangements are particularly opaque”. A Danish

fund added: “We have spent a lot of time getting insight, and have to

a large degree. However, some costs are not very transparent – like

indirect transaction cost.”

Over

half of respondents see value in having a variety of investment

strategies with different time horizons in their fund’s portfolio.

“Multiple strategies – alpha and beta, internal/external, short

term/longer term – should give better results,” said a Danish fund. A

UK fund added: “If you are pursuing unconstrained equity risk-seeking

alpha from manager skill, then you need to have a range of styles or

investment strategies which would include highly concentrated low

turnover portfolios and larger momentum-driven high turnover managers.

| Copyright© 2002-2014 IPE International

Publishers Limited, Registered in England, Reg No. 3233596. |

|