|

August 5,

2014 6:17 pm

Corporate acquirors take early aim at

their target’s investors

By Ed Hammond in New York

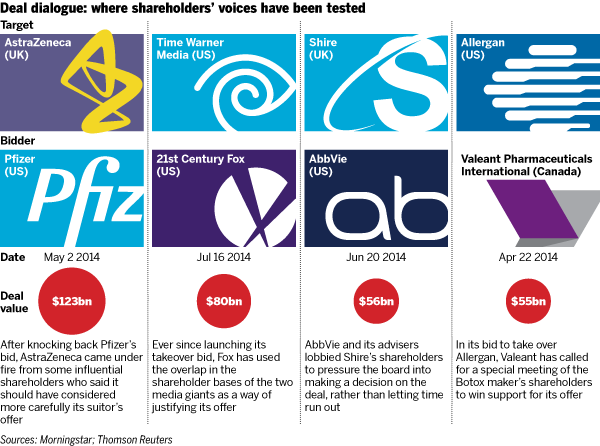

To win investor support for last month’s $53bn takeover of rival drugmaker

Shire,

AbbVie delivered a blunt message to

its target’s shareholders: if you want a deal, speak now or risk us walking

away.

To stress the importance of their response, AbbVie pointed to the example of

AstraZeneca, the UK pharmaceutical

company that in May

fought off attention from US rival

Pfizer – and has faced disgruntled

shareholders ever since.

Abbvie’s tactic worked. Days later – and with its shareholders voicing

support for a deal through the press and directly to its board –

Shire agreed to sell itself to AbbVie.

The willingness of Shire’s shareholders to speak up so early in a takeover

fight highlights a shift in the relationship between companies and their

investors. The shareholder passivity that has long allowed companies to keep

the rump of serious decision making in the boardroom is ebbing.

Increasingly, shareholders want to be part of a wider discussion about what

is best for all those invested in the future of a company. The debate has

been enlivened by the recent surge in dealmaking and activist investment.

At the end of 2013, and with transaction markets still lumbering, the

thought of shareholders interposing their own views on to any M&A

decision-making process was not one stirring many company directors from

sleep.

One example where it did happen was

Charter Communications’ $61bn

unsolicited – and,

ultimately, unsuccessful – offer for

Time Warner Cable. The two US cable

companies had been jousting for a full seven months when T Rowe Price, a top

20 shareholder in TWC, wrote to its board urging it to engage with its

suitor. Even so, the decision to communicate its views directly marked T

Rowe out as a dissenter in an otherwise largely submissive pool of

shareholders.

This year the game has changed: with M&A at healthy levels, shareholders –

and their opinions – have gone from sitting on the sidelines to centre stage

in transactions on both sides of the Atlantic.

The question is why has their role changed?

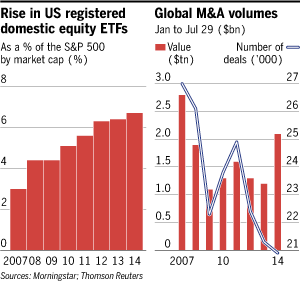

One explanation lies with exchange traded funds. Holding less than 3 per

cent of the market value of the US’s 500 largest public companies five years

ago, ETFs represent about 7 per cent of that shareholder base today. The

increase has coincided with a rich run for funds that passively track the

stock market – the S&P 500 has risen almost 50 per cent in the past three

years. The remainder of publicly traded stock is mostly held by asset

managers, such as BlackRock and T Rowe Price. They, too, have reaped the

fruits of the flourishing market.

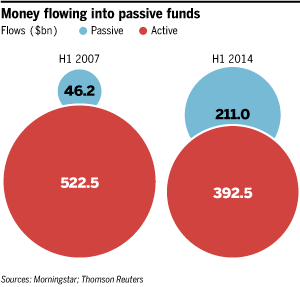

But a big difference between ETFs and asset managers lies in the fees they

charge.

On average, ETFs charge investors an annual fee of 0.47 per cent, whereas

asset managers ask for 1.24 per cent, according to data from Thomson

Reuters.

To justify those higher fees, asset managers cannot passively hold the same

stocks as the ETFs. Instead, they are having to push the companies whose

stock they hold to make better decisions.

Jim Woolery, head of the Shareholder-Director Exchange, a working group that

hopes to foster better discussion between boards and shareholders, says

passivity among asset managers is a thing of the past.

“There has been a tectonic and permanent shift in the American shareholder

base that is creating an economic pressure for asset managers to be more

thoughtful and more vocal about how the companies they invest in should be

run,” said Mr Woolery, who is also chairman-elect of Wall Street law firm

Cadwalader, Wickersham & Taft.

Companies, for their part, seem increasingly willing to listen – and with

good reason. Activist investing and hostile takeover attempts, both of which

have soared this year, prosper when companies and their investors are out of

sync.

“The practice of using investor relations or other arm’s length methods for

speaking to your largest shareholders is fading fast,” says John Studzinski,

global head of Blackstone Advisory Partners. “Chief executives and directors

are realising that they have to be out there themselves, understanding and

addressing the key concerns of shareholders. It is morphing from something

that happens in a crisis towards being accepted best practice.”

An obvious benefit of these pre-event conversations is in learning the right

balance between the competing interests of different investor groups.

As news of deals reach the market, short-term investors known as merger

arbitrageurs often pile into the shares of the target company, betting on

the likelihood of a deal closing. Arbs are typically more vocal than

traditional long-term investors which can put disproportionate pressure on

boards and influence other shareholders to enact decisions that run counter

to what the board sees as being in the best interests of the company.

To defend against this, companies can redefine the rules that govern the

rights of their shareholders.

In July, the board of

Time Warner, the television and film

company (unconnected to Time Warner Cable), changed its bylaws to block its

own investors from forcing it into a $73bn takeover by Rupert Murdoch’s

21st Century Fox. In a move that

reflects that changing pace and degree of shareholder involvement – and the

expectation of it – Time Warner waited just five days after Mr Murdoch’s

public approach before rewriting its rule book.

It was, according to advocates of shareholder-director dialogue, an

indelicate solution to an unnecessary problem. Their hope is that the

increasing tendency of investors to voice their opinions, and of companies

to listen, will lead to decisions that better address the interests of those

stakeholders beyond the boardroom.

|

© The Financial Times Ltd 2014 |

|