The Conference Board

Governance Center Blog

OCT

27

2013

Harvard Law

School Professor

Lucian Bebchuk believes that shareholders should be able to control

the material decisions of the companies they invest in. Over the years, he

has written numerous articles expressing this view, including a 2005

article urging that shareholders should have the power to initiate a

shareholder referendum on material corporate business decisions. In

addition to his writings and speeches, Prof. Bebchuk has established and

directs the Shareholder Rights Project at Harvard Law School for the

purpose of managing efforts to dismantle classified boards and do away

with other charter or bylaw provisions that restrain or moderate

shareholder control of corporations (see “Harvard’s

Shareholder Rights Project is Wrong” and “Harvard’s

Shareholder Rights Project is Still Wrong”). In addition, Prof.

Bebchuk has been at the forefront in arguing to the SEC that, despite the

specific action of Congress in 2010 to empower the SEC to adopt a rule to

require fair and prompt public disclosure of accumulations of shares by

activist hedge funds and other blockholders, the SEC should not do so

because it would limit the ability of activist hedge funds to attack

corporations. In short, Prof. Bebchuk believes that shareholders should

have the power to control the fundamental decisions of corporations – even

those shareholders who bought their shares only a few days or weeks before

they sought to assert their power, and regardless of whether their

investment objective is short-term trading gains instead of long-term

value creation.

While there is no

question that almost every attack, or even rumor of an attack, by an

activist hedge fund will result in an immediate increase in the stock

market price of the target, such gains are not necessarily indicative of

real value creation. To the contrary, the attacks and the efforts by

companies to adopt short-term strategies to avoid becoming a target have

had very serious adverse effects on the companies, their long-term

shareholders, and the American economy. To avoid becoming a target,

companies seek to maximize current earnings at the expense of sound

balance sheets, capital investment, research and development and job

growth. Indicative of the impact of shareholder pressure for short-term

performance is the often cited comment by then-Citigroup CEO Chuck Prince

in the July 9, 2007 Financial Times: “When the music stops, in

terms of liquidity, things will be complicated. But as long as the music

is playing, you’ve got to get up and dance.” Many commentators have cited

pressure to boost short-term performance metrics as one of the causes of

the 2008 fiscal crisis, such as Lynne Dallas in her 2012 article in the

Journal of Corporation Law (“[t]he financial crisis of 2007-2009

was preceded by a period of financial firms seeking short-term profit

regardless of long-term consequences”) and Sheila Bair in her last speech

as FDIC chairman in 2011 (“the overarching lesson of the crisis is the

pervasive short-term thinking that helped to bring it about”). Virtually

all of the academic and government studies of the fiscal crisis have

concluded that shareholder pressure was a contributing cause.

In August of this

year, Prof. Bebchuk released an article describing what he characterized

as empirical evidence that attacks by activist hedge funds do not harm

companies and their long-term shareholders (see “The

Long-Term Effects of Hedge Fund Activism”). I released a paper

pointing out serious deficiencies in the methodology, analysis and

conclusions that Prof. Bebchuk used and I cited an academic study

questioning his statistics, an empirical study to the contrary and

real-world experience and anecdotal evidence that activism and its

concomitant short-termism destroy long-term value and damage the American

economy (see “The

Bebchuk Syllogism”; see also “Current

Thoughts About Activism” and “Bite

the Apple; Poison the Apple; Paralyze the Company; Wreck the Economy”).

Apparently, my paper touched a raw nerve. In an attempt to resuscitate his

promotion and justification of attacks by activist hedge funds, Prof.

Bebchuk has published a new paper (“Don’t

Run Away from the Evidence: A Reply to Wachtell Lipton”) accusing me

of running away from the evidence; a serious accusation, but demonstrably

untrue. Let’s take a look at some of the evidence (empirical,

experiential, and overwhelming) that supports my views.

Empirical

Evidence

It should be

noted that Prof. Bebchuk’s claim that “supporters of the myopic activists

view have failed to back their view with empirical evidence or even to

test empirically the validity of their view” is patently false. In fact,

numerous empirical studies over the years have produced results that

conflict with those Prof. Bebchuk espouses. These other studies generally

find that activism has a negative effect or no effect on long-term value,

particularly when controlling for the skewing impact of a takeover of the

target (which generally occurs at a premium regardless of whether the

target is the subject of activism). This fact compels a careful assessment

and critical review of his study to determine why his results differ from

many prior studies – something I attempted to provide in my previous

paper. I have provided below a brief, and admittedly incomplete, sampling

of such studies.

Director

Contests and Firm Performance

-

According to

Jonathan Macey and Elaine Buckberg in their 2009 “Report on Effects of

Proposed SEC Rule 14a-11 on Efficiency, Competitiveness and Capital

Formation,” there are “[s]everal studies [that] establish that when

dissident directors win board seats, those firms underperform peers by

19 percent to 40 percent over the two years following the proxy

contest.”

-

One of those

studies is David Ikenberry and Josef Lakonishok’s “Corporate Governance

Through the Proxy Contest” (published in the Journal of Business

in 1993), which reviewed 97 director election contests during a 20-year

period in order to examine the long-term performance of targeted firms

subsequent to a proxy contest. Their findings were striking: “When the

incumbent board members successfully retain all board seats, cumulative

abnormal returns are not significantly different from zero over the next

5 years. Yet, in proxy contests where dissidents obtain one or more

seats, abnormal returns following resolution of the contest are

significantly negative. Two years following the contest, the cumulative

abnormal return has declined by more than 20 percent. The operating

performance of these same firms during the postcontest period is also

generally consistent with the pattern observed using stock returns.”

-

Michael Fleming

obtained similar results when looking at instances where a dissident

obtains board representation in “New Evidence on the Effectiveness of

the Proxy Mechanism,” a 1995 Federal Reserve Bank of New York research

paper. Reviewing a sample of 106 threatened proxy contests between 1977

and 1988, Fleming found statistically significant negative returns of

-19.4 percent in the 24 months following the announcement of a contested

election for the 65 firms in his sample where dissidents won board seats

– either as a result of a shareholder vote or a settlement. Fleming

found that the majority of gains resulting from threatened proxy

contests were “attributable to firms which [we]re acquired within one

year of the outcome of the proxy contest,” suggesting that the gains

were due to payment of a takeover premium (consistent with Greenwood and

Schor’s findings described below), not from operating improvements or

governance changes.

-

Lisa Borstadt

and Thomas Zwirlein found very similar results in “The Efficient

Monitoring Role of Proxy Contests: An Empirical Analysis of Post-Contest

Control Changes and Firm Performance,” published in Financial

Management in 1992. These authors examined 142 exchange-traded

firms involved in proxy contests for board representation over a 24-year

period. They found the following: “A dissident victory in the proxy

contest does not necessarily translate into superior corporate

performance. Positive abnormal returns over the proxy contest period are

realized by firms in which the dissidents win the proxy contest and the

firm is subsequently taken over. In contrast, no abnormal performance

over the contest period is observed for the firms in which the

dissidents win but the firm is not subsequently taken over. For these

firms, large negative (although insignificant) cumulative returns are

observed in the postcontest period.”

Shareholder

Proposals and Firm Performance

-

In “Investor

Activism and Takeovers,” published in the Journal of Financial

Economics in 2009, Robin M. Greenwood and Michael Schor examined

Schedule 13D filings by portfolio investors between 1993 and 2006 to

investigate the effect of activist interventions on stock returns. They

found the following: “[A]ctivism targets earn high returns primarily

when they are eventually taken over. However, the majority of activism

targets are not acquired and these firms earn average abnormal returns

that are not statistically distinguishable from zero. . . . Thus, the

returns associated with activism are largely explained by the ability of

activists to force target firms into a takeover, thereby collecting a

takeover premium.”

-

In “Pension

Fund Activism and Firm Performance,” published in the Journal of

Financial and Quantitative Analysis in 1996, Sunil Wahal reviewed

356 “targetings” by the nine most active funds between 1987 and 1993.

“Targetings” included both proxy proposals and nonproxy targeting, and

were typically initiated by sending a letter to the target firm (either

publicly or privately) followed by a telephone call from the activist

fund. Wahal found that, while pension funds “are reasonably successful

in changing the governance structure of targeted firms,” these changes

have no impact on stock performance. According to Wahal, “targeting

announcement abnormal returns are not reliably different from zero,” and

“[t]he long-term abnormal stock price performance of targeted firms is

negative prior to targeting and still is negative after targeting.”

Wahal also found that “accounting measures of performance do not suggest

improvements in operating or net income either; accounting measures of

performance also are negative prior to and after targeting.”

-

Two studies

released by the U.S. Chamber of Commerce in partnership with Navigant

Consulting reviewed shareholder proxy proposals between 2002-2008 and

2009-2012, respectively, for impact on firm performance. The studies,

published in May 2009 and May 2013, both focused on shareholder

proposals that were identified as “Key Votes” by the AFL-CIO in annual

surveys during the respective time periods, including proposals

reflecting board declassifications, proxy access and director removal

policies. In the first study, “Analysis of the Wealth Effects of

Shareholder Proposals – Volume II,” Joao Dos Santos and Chen Song

reviewed 166 shareholder proposals between 2002-2008 and found “no

evidence of a statistically significant overall short-run or long-run

improvement and some indication of a long-run decrease in market value

for the firms in our sample.” In the second study, “Analysis of the

Wealth Effects of Shareholder Proposals – Volume III,” which reviewed 97

shareholder proposals between 2009-2012, Allan T. Ingraham and Anna

Koyfman came to similar conclusions: “We . . . find no conclusive or

pervasive evidence that the shareholder proposals assessed in this study

improve firm value or result in an economic benefit to pension plans and

plan participants. Given that the proxy process imposes costs on both

firms and shareholders, and given that there are no proven benefits in

terms of corporate performance, the overall net benefit of these

initiatives is likely negative.”

-

Andrew K.

Prevost and Ramesh P. Rao studied the impact of shareholder activism by

public pension funds in their paper “Of What Value Are Shareholder

Proposals Sponsored by Public Pension Funds?” (published in the

Journal of Business in 2000), examining a total of 73 firms that

received shareholder proposals during the period of 1988-1994. They came

to the following conclusions: “Firms that are subject to shareholder

proposals only once during the sample period experience transitory

declines in returns, but firms that are subject to repeat shareholder

proposals experience permanent declines in market returns. . . .

Long-term changes in operating performance corroborate the event study

results: firms targeted only once exhibit positive but insignificant

long-term results, while those targeted repeatedly show strong declining

performance.”

-

Jonathan M.

Karpoff, Paul H. Malatesta and Ralph A. Walkling reviewed 522

shareholder proposals at 269 companies between 1986 and 1990 to

determine the impact of shareholder proposals on firm performance in

“Corporate Governance and Shareholder Initiatives: Empirical Evidence,”

published in the Journal of Financial Economics in 1996. After

finding that “proposals are targeted at poorly performing firms,” they

concluded that, notwithstanding this fact, the “average effect of

shareholder corporate governance proposals on stock values is close to,

and not significantly different from, zero.” In fact, “[s]ales growth

declines for firms that receive proposals in relation to sales growth

for control firms,” “[c]hanges in operating return on sales are not

significantly larger for proposal firms than their controls, and are not

significantly related to the persistence or intensity of proposal

pressure, or to the sponsors’ identity,” and “[c]hange in operating ROA

are not related to the pressure’s intensity or sponsors’ identity.”

-

In “Less is

More: Making Institutional Shareholder Activism a Valuable Mechanism of

Corporate Governance,” published in the Yale Journal on Regulation

in 2001, Yale Law School professor Roberta Romano conducted a review of

the corporate finance literature on institutional investors’ corporate

governance activities, involving seven different empirical studies and a

total of over 4,500 individual shareholder proposals. She found that the

shareholder proposals had “little or no effect on targeted firms’

performance” over the time periods considered in the studies and

proposed that improvements might be achieved if the rules were revised

“to require proposal sponsors either to incur the full cost of a losing

proposal or a substantial part of the cost.”

-

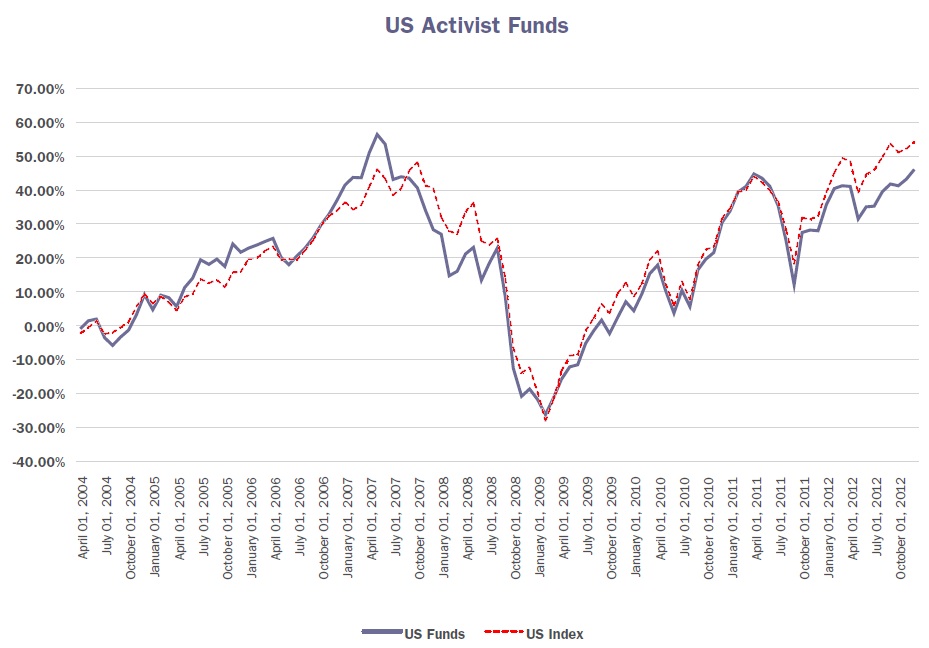

It is

particularly noteworthy that CalSTRS, one of the major public employee

pension funds and one of the leaders in proxy voting and investing in

activist hedge funds, has recently reported that its aggregate

investments in activist funds as of October 2012 trailed the United

States public equity market, as shown by this chart from its annual

report.

US Activist Funds 2004 – 2012

If activist funds

fail to achieve attractive returns for their own investors, it raises the

question whether pension funds and other fiduciary investors are actually

promoting the best interests of the beneficiaries of the funds they manage

when they invest in activist funds, given the fact that activist funds

promote short-termism with its attendant costs to the rest of the market

and to the economy as a whole (see Leo E. Strine’s “One Fundamental

Corporate Governance Question We Face: Can Corporations Be Managed for the

Long Term Unless Their Powerful Electorates Also Act and Think Long Term,”

published in The Business Lawyer in November 2010). This month

the UK Law Commission published a consultation paper responding to a

government request, based on the Kay Review discussed below, “To evaluate

whether fiduciary duties (as established in law or as applied in practice)

[of investment intermediaries] are conducive to investment strategies in

the best interests of the ultimate beneficiaries. We are asked to carry

out this evaluation against a list of factors, balancing different

objectives, including encouraging long-term investment strategies

[emphasis supplied] and requiring a balance of risk and benefit.”

Takeover

Defenses and Firm Value

-

Approaching the

question from another perspective, William C. Johnson, Jonathan M.

Karpoff and Sangho Yi investigated the impact of takeover defenses on

firm value in “The Bonding Hypothesis of Takeover Defenses: Evidence

from IPO Firms” (April 29, 2013 working paper, available at

http://papers.ssrn.com/abstract=1923667). Looking at a sample of

1,219 firms that went public between 1997 and 2005, the authors tested

the “bonding hypothesis of takeover defenses” – that is, the theory that

“takeover defenses increase the value of managers’ commitments to

maintain their promised operating strategy and not to opportunistically

exploit their counterparties’ investments in the IPO firm,” which, “in

turn, encourages the firm’s counterparties to invest in the business

relationship, yielding benefits for the IPO firm.” The authors reported

the following findings:

(1) IPO firms deploy more takeover defenses

when they have large customers, dependent suppliers, or strategic

partners;

(2) The IPO firm’s value is positively related to its use of takeover

defenses, particularly when it has large customers, dependent suppliers,

and/or strategic partners;

(3) The IPO firm’s subsequent operating performance is positively related

to its use of takeover defenses, particularly when it has large customers,

dependent suppliers, and/or strategic partners;

(4) When the IPO firm announces its intention to go public, its large

customers experience a change in share values that is positively related

to the IPO firm’s use of takeover defenses; and

(5) After the IPO, the longevity of the IPO firm’s business relationship

with its large customer is positively related to its use of takeover

defenses.

According to the authors, these results are

explained by the fact that “takeover defenses … help to economize on the

cost of building and maintaining value-increasing trading relationships

between the IPO firm and its counterparties.” As a result, “at IPO firms

whose values depend heavily on their relationships with customers,

suppliers, and strategic partners, takeover defenses appear to increase

value by bonding the IPO firm’s commitment to these relationships.”

-

In “The Impact

of Antitakeover Amendments on Corporate Financial Performance”

(published in The Financial Review in 2001), Mark S. Johnson

and Ramesh P. Rao examined a sample of 649 antitakeover amendments

adopted between 1979 and 1985 to determine the impact of the passage of

antitakeover amendments on firm share price. Contrary to the management

entrenchment hypothesis, the authors found that “antitakeover amendments

are relatively benign events that do not significantly impact managerial

behavior,” and that “antitakeover amendments are not associated with

deleterious effects to shareholders in terms of their impact on various

fundamental firm performance measures.”

Managerial

Behavior and Pressures to Achieve Short-Term Performance

-

Jie He and Xuan

Tian’s “The Dark Side of Analyst Coverage: The Case of Innovation”

(forthcoming in the Journal of Financial Economics) examined

the effect of analyst coverage on firm innovation to investigate how the

pressure to achieve short-term performance impacts managerial behavior.

The short-term pressures exerted by activist investors are often no

different than those generated by stock analysts, and in many instances

activist investors merely piggyback on stock analyst commentary when

they launch attacks. Examining a sample of 25,860 firm-year observations

relating to U.S. listed firms during the period of 1993-2005, He and

Tian explored the “innovation output” of firms (as measured in terms of

the number of (i) patent applications filed in a given year that are

eventually granted and (ii) non-self citations each patent receives in

subsequent years) in relation to the intensity of analyst coverage (as

measured by the average number of earnings forecasts issued for the firm

each month). The authors found that “an exogenous average loss of one

analyst following a firm causes it to generate 18.2 percent more patents

over a three-year window than a similar firm without any decrease in

analyst coverage” and that “an exogenous average loss of one analyst

following a firm leads it to generate patents receiving 29.4 percent

more non-self citations than a similar firm without any decrease in

analyst coverage.” He and Tian determined that this evidence “is

consistent with the hypothesis that analysts exert too much pressure on

managers to meet short-term goals, impeding firms’ investment in

long-term innovative projects.”

-

Natalie Mizik

published similar findings in “The Theory and Practice of Myopic

Management,” featured in the Journal of Marketing Research in

2010. In this study, Mizik reviewed the operating performance, marketing

spending, R&D spending and stock price performance of 6,642 firms

between 1986 and 2005 to assess the financial consequences of the

practice of cutting marketing and R&D spending to inflate short-term

earnings. In order to isolate firms that were potentially engaging in

“myopic management,” Mizik filtered for firms that simultaneously

reported greater-than-normal profits, lower-than-normal marketing

expenses and lower-than-normal R&D spending. Mizik then compared the

stock performance of these “potentially myopic” firms against the

performance of “nonmyopic” firms. Potentially myopic firms initially

experienced much better stock performance than the firms that failed to

meet performance expectations. However, after four years, “the portfolio

of potentially myopic firms ha[d] a negative return of -15.7 percent,

far below the return to the two nonmyopic benchmark portfolios (29.2

percent and 13.3 percent) and the S&P 500 return of 21.6 percent.” Mizik

concludes that “[m]yopic management might have some short-lived benefits

– it leads to higher current-term earnings and stock price – but it

damages the long-term financial performance of the firm because the

initial gains are followed by greater negative abnormal returns.”

-

Aleksandra

Kacperczyk’s “With Greater Power Comes Greater Responsibility?”

(published in the Strategic Management Journal in 2009) tested

the effect of takeover protection on the amount of corporate attention

paid to shareholders and non-shareholding stakeholders, respectively.

Looking at a sample of 878 firms between 1991 and 2002, Kacperczyk found

that “an exogenous increase in takeover protection leads to higher

corporate attention to community and the natural environment, but has no

impact on corporate attention to employees, minorities and customers,”

and that “firms that increase their attention to stakeholders experience

an increase in long-term shareholder value,” measured over the two-year

and three-year periods following the increase in takeover protection.

-

Other empirical

studies have shown that pressure from investors with short investment

horizons can influence management to engage in financial misreporting.

In “Institutional Ownership and Monitoring: Evidence from Financial

Misreporting” (published in the Journal of Corporate Finance in

2010), Natasha Burns, Simi Kedia and Marc Lipson examined a sample of

firms that restated their earnings between 1997 and 2002, finding that

ownership by “transient institutions” (those with short investment

horizons) are positively related with an increase in the likelihood and

severity of an accounting restatement. The authors concluded that “[i]t

is precisely these institutions, which trade frequently and therefore

are likely to focus management attention on short-term reported

performance, that provide incentives to manipulate earnings.”

-

Another

relevant study coming out of the financial crisis examined whether the

corporate governance characteristics of banks impacted the likelihood of

banks requiring government “bailout” support during the financial

crisis. In “Shareholder Empowerment and Bank Bailouts” (a 2012 working

paper), Daniel Ferreira, David Kershaw, Tom Kirchmaier and Edmund

Schuster created a “management insulation” index ranking the degree of

banks’ management insulation based on their charter and by-law

provisions and on the provisions of the applicable state corporate law

that make it difficult for shareholders to oust management. They found

that, in a sample of U.S. commercial banks, banks in which managers are

“fully insulated” from shareholders were roughly 19 to 26 percentage

points less likely to receive state bailouts than banks whose managers

were subject to stronger shareholder rights. The authors explained that

“[b]ank shareholders may have incentives to increase risk taking beyond

the socially-optimal level” and that, “in search for higher returns,

bank shareholders had incentives to push their banks towards less

traditional banking activities.”

-

In his article

“Do Institutional Investors Prefer Near-Term Earnings Over Long-Run

Value?” (published in Contemporary Accounting Research in

2001), Brian Bushee examined a sample of 10,380 firm-years between 1980

and 1992 to determine whether institutional investors exhibit

preferences for near-term earnings over long-run value. Bushee found

that “the level of ownership by institutions with short investment

horizons (transient institutions) and by institutions held to stringent

fiduciary standards (banks) is positively (negatively) associated with

the amount of value in near-term (long-term) earnings.” Bushee found no

evidence that banks “myopically price” firms by overweighting short-term

earnings potential and underweighting long-term earnings potential.

However, in transient institutions “high levels of transient ownership

are associated with an over- (under-) weighting of near-term (long-term)

expected earnings and a trading strategy based on this finding generates

significant abnormal returns. This finding supports the concerns that

many corporate managers have about the adverse effects of an ownership

base dominated by short-term-focused institutional investors.”

-

The above

result is consistent with an earlier empirical study by Bushee that

examined the influence of shareholder demographics on earnings

management by managers. In “The Influence of Institutional Investors on

Myopic R&D Investment Behavior,” published in the Accounting Review

in 1998, Bushee investigated whether institutional investors create or

reduce incentives for corporate managers to reduce investment in

research and development to meet short-term earnings goals. Examining a

sample of all firm-years between 1983 and 1994 with available data,

Bushee found that “a high proportion of ownership by institutions

exhibiting transient ownership characteristics (i.e., high

portfolio turnover, diversification, and momentum trading) significantly

increases the probability that managers reduce R&D to boost earnings.”

Bushee believed that “[t]his result supports the widely-argued view that

short-term-oriented behavior by institutions creates pressures for

managers to sacrifice R&D for the sake of higher current earnings” among

those firms with high levels of transient ownership.

-

William Pugh,

Daniel Page and John Jahera, Jr.’s “Antitakeover Charter Amendments:

Effects on Corporate Decisions” (published in the Journal of

Financial Research in 1992) tested whether managers adopt a

longer-term investment strategy after their firm passes antitakeover

charter amendments. Examining a sample of firms that adopted

antitakeover charter amendments between 1978 and 1985, the authors found

that “firms increase spending on fixed capital as a percentage of both

sales and assets the year of passage and for several years thereafter,”

and that overall results with respect to R&D expenditures “appear to

support the managerial myopia hypothesis.”

-

A recent survey

of 1,038 board members and executives by McKinsey & Company and the

Canada Pension Plan Investment Board found startling levels of

short-term orientation among corporate executives. As reported in the

Wall Street Journal on May 22, 2013, this study found the

following:

- 63 percent of business leaders indicated the

pressure on their senior executives to demonstrate strong short-term

financial performance has increased in the past five years.

- 79 percent of directors and senior executives said they felt the most

pressure to demonstrate strong financial performance over a time period of

less than two years. Only seven percent said they felt pressure to deliver

strong financial performance over a horizon of five or more years.

- However, respondents identified innovation and strong financial returns

as the top two benefits their company would realize if their senior

executives took a longer-term view to business decisions.

- Yet, almost half of respondents (44 percent) said that their company’s

management team currently uses a primary time horizon of less than three

years when they conduct a formal review of corporate strategy. 73 percent

said this primary time horizon should be more than three years and 11

percent said the horizon should be more than 10 years.

-

The McKinsey

findings are consistent with an earlier study published in the

Financial Analysts Journal in 2006. In “Value Destruction and

Financial Reporting Decisions,” John Graham, Campbell Harvey and Shiva

Rajgopal described the results of a survey of 401 senior financial

executives. Going a step further than the McKinsey study, the authors

asked executives if they would be willing to sacrifice long-term value

in order to smooth earnings. An “astonishing 78 percent admit[ted] they

would sacrifice a small, moderate or large amount of value to achieve a

smoother earnings path.”

Short-Termism

and Macroeconomic Productivity

The problems

discussed above have larger implications than simply the performance of

individual firms. In his 2012 book, Corporate Law and Economic Stagnation:

How Shareholder Value and Short-Termism Contribute to the Decline of the

Western Economies, Pavlos Masouros used macroeconomic data to show that

the shift in corporate governance toward shareholder interests and

increasing short-termism in France, Germany, the Netherlands, the UK and

the US have contributed to low GDP growth rates in those countries since

the early 1970s. Masouros outlined the unfolding of a “Great Reversal in

Corporate Governance” whereby the primacy of shareholder value in the

corporate governance pecking order was established, as well as a “Great

Reversal in Shareholdership” where the average holding period of shares

rapidly decreased, both of which contributed to a dramatic increase in the

average equity-payout ratio of firms and a decrease in the average capital

retention and reinvestment of profits by firms. Masouros’ prescription for

ameliorating this trend away from capital reinvestment is what he calls

“Long Governance” – moving toward a system where shareholders are infused

with incentives that would allow them to develop long-term horizons that

would align their interests with other constituencies and increase

companies’ incentives to invest in future productivity.

In “The Kay

Review of UK Equity Markets and Long-Term Decision Making,” published by

the UK Department for Business Innovation and Skills in July 2012 (the

“Kay Review”), John Kay examined how the structure of the UK equity

markets encourages short-termism and discussed the impact on UK businesses

and investors. Kay started with the observation that “[a]s a percentage of

GDP, research and development expenditure by British business has been in

steady decline” and proceeded to explore why this was the case. He then

identified a fundamental misalignment of the interests of the UK asset

management industry and the ultimate principals, the companies which use

equity markets and the individual UK “savers” who provide funds to them:

“Returns to beneficial owners, taken as a whole, can be enhanced only by

improving the performance of the corporate sector as a whole. Returns to

any subset of beneficial owners can be enhanced, at the expense of other

investors, by the superior relative performance of their own asset

managers. Asset managers search for alpha, risk adjusted outperformance

relative to a benchmark. But savers collectively will earn beta, the

average return on the asset class.” This misalignment exists because “the

time horizons used for decisions to hire or review investment managers are

generally significantly shorter than the time horizon over which the

saver, or the corporate sponsor of a pension scheme, is looking to

maximize a return.” Kay pointed out that “[c]ompetition between asset

managers to outperform each other by anticipating the changing whims of

market sentiment … can add nothing, in aggregate, to the value of

companies … and hence nothing to the overall returns to savers.”

Predictably, the short-term incentives of asset managers flow down to

corporate managers, many of whom are incentivized “to make decisions whose

immediate effects are positive even if the long run impact is not” and

“whose consequences are likely to be apparent within a short time scale.”

After describing the problem in great detail, Kay presented a series of

recommendations that he believed “will help to deliver the improvements to

equity markets necessary to support sustainable long-term value creation

by British companies,” including the recommendation that “regulation must

be directed towards the interests of market users – companies and savers –

rather than the concerns of market intermediaries.” The applicability of

Kay’s analysis to American equity markets is obvious.

The

Evidence of Experience

No matter how

much Professor Bebchuk attempts to denigrate what he calls “anecdotal”

evidence, the experiences of those with “boots on the ground” must be

taken into consideration in combination with the empirical evidence

sampled above. Take, for example, some of the statements below from

leaders who have firsthand experience with the short-term pressures faced

by public company managers and directors.

Bill George, a

professor at Harvard Business School, former chief executive of the

medical device company Medtronic, and currently a director of Goldman

Sachs and Exxon Mobil, recently said in his August 2013 New York Times

article, Activists Seek Short-Term Gain, Not Long-Term Value:

“While activists often cloak their demands in the language of long-term

actions, their real goal is a short-term bump in the stock price. They

lobby publicly for significant structural changes, hoping to drive up the

share price and book quick profits. Then they bail out, leaving corporate

management to clean up the mess. Far from shaping up these companies, the

activists’ pressure for financial engineering only distracts management

from focusing on long-term global competitiveness.”

Warren Buffet and

27 other highly regarded businesspeople, academics, investment bankers and

union leaders expressed concerns about short-termism in “Overcoming Short-Termism:

A Call for a More Responsible Approach to Investment and Business

Management,” a 2009 Aspen Institute policy statement. In this paper, these

leaders voiced concern that “boards, managers, shareholders with varying

agendas, and regulators, all, to one degree or another, have allowed

short-term considerations to overwhelm the desirable long-term growth and

sustainable profit objectives of the corporation,” and that this trend

toward short-term objectives has “eroded faith in corporations continuing

to be the foundation of the American free enterprise system.” In

particular, they noted that “the focus of some short-term investors on

quarterly earnings and other short-term metrics can harm the interests of

shareholders seeking long-term growth and sustainable earnings, if

managements and boards pursue strategies simply to satisfy those

short-term investors,” which “may put a corporation’s future at risk.”

Dominic Barton,

global managing director of McKinsey & Company, described the problem in

“Capitalism for the Long-Term,” a 2012 McKinsey publication: “[E]xecutives

must do a better job of filtering input and should give more weight to the

views of investors with a longer-term, buy-and-hold orientation. . . . If

they don’t, short-term capital will beget short-term management through a

natural chain of incentives and influence. If CEOs miss their quarterly

earnings targets, some big investors agitate for their removal. As a

result, CEOs and their top teams work overtime to meet those targets. The

unintended upshot is that they manage for only a small portion of their

firm’s value. When McKinsey’s finance experts deconstruct the value

expectations embedded in share prices, we typically find that 70 to 90

percent of a company’s value is related to cash flows expected three or

more years out. If the vast majority of most firms’ value depends on

results more than three years from now, but management is preoccupied with

what’s reportable three months from now, then capitalism has a problem.”

Daniel Vasella,

former chairman and CEO of Novartis AG, spoke firsthand about the

pernicious effects of the pressure created by such short-term expectations

in a 2002 Fortune article: “Once you get under the domination of

making the quarter – even unwittingly – you start to compromise in the

gray areas of your business, that wide swath of terrain between the top

and bottom lines. Perhaps you’ll begin to sacrifice things (such as

funding a promising research-and-development project, incremental

improvements to your products, customer service, employee training,

expansion into new markets, and yes, community outreach) that are

important and that may be vital for your company over the long term.”

A

Proposal for Effective Shareholder Engagement

In laying out the

evidence above, I do not mean to say that all forms of investor engagement

are bad. To the contrary, I believe that collaborative interaction between

boards and long-term shareholders can help increase the effectiveness of

boards. Consider the observations of John Kay in the Kay Review. Kay

encouraged “effective engagement” between asset managers and the companies

they invest in. However, he did not hold all forms of engagement equal,

arguing instead that all participants in the equity investment chain

should act according to the principles of what he calls “stewardship”:

“Our approach, which emphasizes relationships based on trust and respect,

rooted in analysis and engagement, develops and extends the existing

concept of stewardship in equity investment. This extended concept of

stewardship requires that the skills and knowledge of the asset manager be

integrated with the supervisory role of those employed in corporate

governance: it looks forward to an engagement which is most commonly

positive and supportive, and not merely critical.” Kay recommends that

company directors “facilitate engagement with shareholders, and in

particular institutional shareholders such as asset managers and asset

holders, based on open and ongoing dialogue about their long-term concerns

and investment objectives.” But, importantly, he also emphasizes that

directors should “not allow expectations of market reaction to particular

short-term performance metrics to significantly influence company

strategy.”

I support Kay’s

views on what constitutes “effective engagement” and believe shareholder

collaboration with management and directors along these lines could be a

value-enhancing development for many companies both in the short-run and

long-run.

Standing

Firm, Not Running Away

As to Professor

Bebchuk’s allegation, I think it is clear that, far from “running away”

from the evidence, my views and my colleagues’ views are supported by many

highly respected academics, policymakers, investors and business leaders

whose empirical analyses and real-world experiences show that most

activist interventions contribute to managerial short-termism and harm the

innovation and growth potential of American companies. It is also clear

that empirical evidence must be considered in context with other forms of

evidence, including macroeconomic analysis, real-world experience and

common sense, to determine if it tells a story that makes sense in the

real world.

|

About the Guest Blogger:

|

Marty Lipton, Wachtell, Lipton, Rosen & Katz |

|

Martin Lipton, a founding partner of

Wachtell, Lipton, Rosen & Katz, specializes in advising major

corporations on mergers and acquisitions and matters affecting

corporate policy and strategy and has written and lectured

extensively on these subjects.

This

post originally appeared as a Wachtell Lipton memo on October 25,

2013. |

© 2013 The Conference Board Inc. |