|

|

Photograph by Jeremy Liebman for Bloomberg Businessweek

“I like the thrill of the hunt” |

Stocks

Ryan

Morris, 28-Year-Old Activist Investor

By

Karen Weise

on December 20, 2012

Ryan Morris spent a week steeling himself for the showdown. Then 27 years

old, he was in his first campaign as an activist investor, trying to wrest

control of a small company named InfuSystem (INFU),

which provides and services pumps used in chemotherapy. In the meeting,

Morris would confront InfuSystem’s chairman and vice chairman, two men in

their 40s, and tell them that as a shareholder, he thought the company was

heading in the wrong direction.

Morris is competitive—his high school rowing teammates nicknamed him “Cyborg,”

and he took a semester off college to race as a semi-pro cyclist—but

face-to-face confrontation wasn’t something he relished. “I like the

thrill of the hunt, but not the kill,” he says. To prepare, Morris

outlined questions, guessed potential responses, and tried to anticipate

what tense “pregnant moments” could arrive. He built his clout by lining

up support from InfuSystem’s largest shareholder as well as a veteran

activist investor. Morris knew his own looks—he resembles a sandy-haired

Mitt Romney—could help mask his youth, and decided he’d wear a tie, much

as he hates to.

The company, with just $47 million in revenue, was spending too much

money, and in the wrong places. In the previous year, InfuSystem’s board

and CEO earned more than $11 million combined. This was for a company

whose stock had lost 40 percent of its value over the previous three

years. Morris figured that as a shareholder voice on the board, he could

help cut expenses—including the high pay—and, once it was clean enough to

sell, reap a return for his own small hedge fund.

On Dec. 13, 2011, he finally sat at a conference table across from the two

directors. After 45 minutes of discussion, he still didn’t think his

concerns were being acknowledged. So he got to the point: He wanted three

board seats.

When an activist investor like Carl Icahn tries to take over a household

brand, it plays out on CNBC. Most shareholder struggles occur when

little-known investment funds try to take over little-known companies like

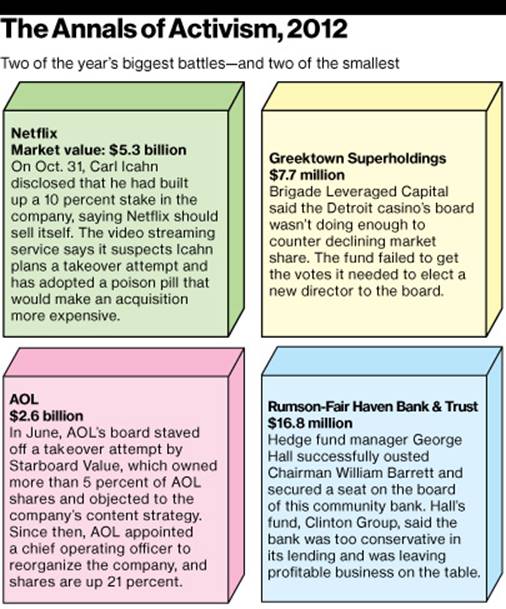

InfuSystem. Of the more than two dozen activist battles in 2012, most

involved companies with a market value under $50 million. In the smallest

face-off this year, Georgetown Law student Daniel Rudewicz, 29, tried and

failed to gain control of a $2.2 million company that makes microwave

filters.

Many of the fights are being waged by a younger generation of activists,

according to Ron Berenblat, Morris’s attorney at Olshan Frome Wolosky.

Among the firm’s clients is a 24-year-old about to start his first

activist campaign, trying to take over a technology company. Morris’s

experience, says Berenblat, puts him “on the new forefront of

30-and-younger activist investors who are intelligent, patient, and

highly methodical.” After the financial crisis exhausted even the most

seasoned investors, young activists like Morris are bringing new energy to

the hunt, shining light into dark corners of the market that are often

overlooked.

Growing up in Toronto, Morris dreamed of becoming a nuclear physicist,

obsessed with the idea that nuclear fusion could create infinite, clean

energy—that was, until his father let him in on some bad news. “Even if

you become the best scientist in the world, you will not make fusion

happen,” Ryan recalls him warning. “If you want to make something happen,

you need to be in charge of capital. It’s the resource allocation that

gets things done.”

Morris started reading Warren Buffett’s Berkshire Hathaway (BRK/A)

shareholder letters. To the 12-year-old Morris, it seemed so easy: With

hard work and a clear mind, an independent thinker could spot an

undervalued company, buy it cheap, and hold on until other investors

recognize the company’s true worth. “Something where you can do well while

being a loner was kind of appealing,” he says.

Using money from a summer job laying lawn sprinklers, Morris soon bought

his first stock, a company that made fuel cells. He kept investing when he

moved to upstate New York to study operations research at Cornell

University and later as he extended his undergraduate degree into a

master’s in engineering. Alongside classes and cycling, Morris worked with

fellow student Paul George to found a profitable company called VideoNote

that made it easy for Cornell to stream lectures online. As graduation

loomed, Morris decided he didn’t want to take a job on Wall Street, where

he could earn millions in the algorithm-driven world of quantitative

finance. The financial models that drive the market’s split-second trades

were “dumb” in Morris’s eyes, George says. “His whole position is take

long-term positions on companies and don’t try to trade on noise. You

can’t predict anything.”

He still wanted to be an investor, though. In the fall of 2008, with the

stock market in freefall, and lots of companies at historic lows, Morris

saw an opportunity. By early 2009 he was talking with George about

managing his money, with a compelling pitch: “He said, ‘Cast aside your

emotions. … People are overreacting, so I can come in and be rational,’ ”

George recalls. George handed over some of their payout from VideoNote and

a small inheritance, becoming Morris’s first investor. With their combined

$50,000, Morris opened his fund on Feb. 24, 2009, naming it Meson Capital

Partners after a subatomic particle. His timing was perfect: The stock

market bottomed in March and has more than doubled since.

Over the coming months, Morris sent some close friends and professors a

10-page letter detailing his value approach, which embodied Buffett’s idea

of investing in companies that have strong business prospects and are not

simply hot stocks. A few gave him money, and a single question Morris

asked of Berkshire Hathaway Vice Chairman Charlie Munger at Wesco

Financial’s annual meeting helped him pull in more. He asked whether it’s

harder to pursue a “buy and hold” strategy when businesses seem to evolve

faster and faster. Ben Claremon, a blogger who circulated a transcript of

the meeting, noted next to Morris’s name: “Watch out for this guy: Some

very smart people think he is going to be a star fund manager.”

Morris didn’t start out as an activist. At first he looked for sound

companies that had been swept up in the market panic and noticed that some

small aircraft leasing companies had taken a beating. “If you think of a

headline for an investment that involves ‘airlines’ and ‘finance’ you can

imagine there was not much competition in buying these stocks,” Morris

would write to investors. He invested about 40 percent of his fund in

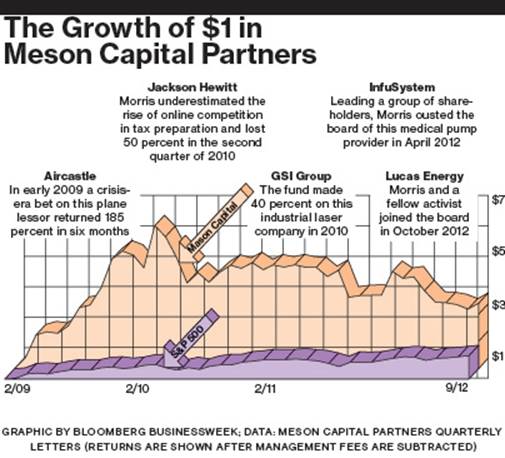

three companies and the stocks soared. By the end of the year, Morris’s

fund had gained 753 percent before fees—17 times the return of the

Standard & Poor’s 500-stock index. In his first annual letter, he told his

investors this was “embarrassingly far off our target” of beating the S&P

by 10 percent annually over three to five years. “This was not a

sustainable performance.”

The returns attracted great interest, some of which Morris calls “the

wrong kind of attention.” One potential investor asked, “OK, I will get

50 percent a year, right?” Morris says he turned away several of these hot

money types. His letters, which laid out his strategies, started making

the rounds among well-known value investors and eventually landed in the

hands of Whitney Tilson, founder of hedge fund T2 Partners. “There’s this

young guy who looks off the beaten path for interesting, misplaced

situations,” Tilson says. And those returns? “That catches anyone’s eye.”

In 2010, Tilson and Zeke Ashton, founder of Centaur Capital Partners,

became seed investors in Morris’s partnership, providing a bit of capital

and a regular source of advice.

Morris’s second year didn’t match his first. In the words of his next

annual letter, it was “marked by frustration and underperformance.” There

were some bright spots when he “coat tailed” the work of other activist

investors. One forced a bloated pharmaceutical company to sell itself, and

another managed to wring some money for shareholders out of an industrial

laser business reorganizing in bankruptcy. Reflecting on the year, Morris

told his investors that the success of those activists made him optimistic

about his own future, writing, “Hopefully, as we grow in the future, we

can be the ones to save the day.”

“Why did he become an activist investor? Because he got screwed,” George

says. In early 2011, Morris invested in a hearing aid provider called

HearUSA, which he thought was undervalued after it signed a long-delayed

deal with AARP. Then HearUSA’s largest supplier, Siemens (SI),

forced the company to file for bankruptcy protection over a contract

dispute. Morris says he was caught totally off guard—he’d seen no warning

signs in the hundreds of pages of filings he’d read—and sold 80 percent of

his shares at a loss.

After reading more documents from the case, Morris decided that HearUSA’s

business was sound and that Siemens acted because it was at odds with the

company’s management. As HearUSA’s stock fell in the wake of the

bankruptcy filing, Morris began buying shares, paying on average a third

of what he paid for his original stake. He then joined other investors in

persuading the bankruptcy trustee to establish an equity committee to

represent shareholders. Morris and the rest of the committee helped

negotiate a deal for Siemens to buy HearUSA, avoiding liquidation and

doubling Meson’s total investment.

As that foray ended, a HearUSA shareholder tipped Morris off to InfuSystem.

The company had a steady, recurring revenue stream. After all, “cancer

treatment services are totally economically insensitive,” says Morris. “If

Europe crashes, you still need this service.” But that cash flow was

obscured by what Morris politely calls “nonessential costs.” In 2010 the

board awarded $7.2 million in salary, stock, and other compensation to

Chairman and Chief Executive Officer Sean McDevitt, gave $1.3 million to

Vice Chairman Pat LaVecchia, and awarded at least $400,000 to almost every

other member of the board, according to Securities and Exchange Commission

filings. It let the stock awards vest immediately and had InfuSystem pay

the personal income taxes they triggered. That meant InfuSystem’s board

earned six times the median compensation for other micro-cap companies,

according to data from the National Association of Corporate Directors.

Reading the filings, Morris questioned how the board, which included

pharmaceutical executives and an astronaut, could approve the largess.

“These don’t seem like bad people,” he thought. (Members of the board did

not respond to requests for comment for this article.)

Fresh off his experience with HearUSA, Morris thought if he could get a

voice on the board, he could help investors. He says he called the largest

shareholders and learned they were irked too. That’s when Morris began

laying the groundwork for battle. He bought 2 percent of InfuSystem’s

shares and persuaded Kleinheinz Capital Partners, the company’s largest

shareholder, and veteran small-cap activist Chuck Gillman to join him in

an official group of concerned shareholders. On Dec. 6, 2011, Morris filed

a form called a Schedule 13D with the SEC, declaring the group controlled

11.4 percent of InfuSystem’s shares and intended to influence the board.

In the face-to-face meeting a week later, Morris says McDevitt and

LaVecchia defended the stock awards, explaining that the board wanted to

boost the company’s market capitalization so it could move from trading on

over-the-counter exchanges to the NYSE Amex. Morris says that when he

raised the prospect of joining the board, McDevitt’s face reddened as he

sarcastically retorted, “Oh, we’d love to spend more time with you.”

Five days later, Morris learned the board rejected the shareholders’

request for three seats. He scoured InfuSystem’s bylaws and decided to

demand a “special meeting,” which management must call within 75 days

after a majority of all shareholders demand one. Morris was confident he

could get the support he needed, and on Jan. 18, 2012, filed a preliminary

proxy statement calling for the special meeting to replace the board.

This is about the time when many shareholder activists would start firing

off nasty press releases attacking current management as corrupt or

incompetent in an effort to rally shareholder support. Such battles can

escalate quickly and end up in court. Morris says, “as much as I love

lawyers, I don’t really love paying them.” Instead, he issued what he

calls “gentlemanly” press releases that announced his SEC filings.

When Morris called shareholders, some said, “Thank God you’re here.”

Others were skeptical. How did they know that Morris wouldn’t raid the

company for himself? “I was like, ‘I’m 27. I would be ending my career

right now if I was going to do that,’ ” he recalls. By March 5, Morris’s

group had more than the 50 percent support needed. The InfuSystem board

now had until May 7 to call the special meeting.

McDevitt and the board began negotiating. In

the final deal, McDevitt, LaVecchia, and all but two of the board members

were out. “I fired an astronaut,” Morris says now with a slight smile.

McDevitt waived the 2 million shares he was entitled to under his

employment contract and instead took a $1 million payout. “If we had had

nasty press releases, there’s no way we would have settled that severance

thing,” Morris says. InfuSystem would get a new CEO and seven new board

members, with Morris as the chairman, one of the youngest on the NYSE. “I

am two months younger than Zuckerberg,” he says. “But he’s about a zillion

dollars richer.”

On a November afternoon in Manhattan, Morris sat at a desk stacked with

moving boxes and explained that he was closing InfuSystem’s New York

office. InfuSystem had leased the office for McDevitt and a team of

financial analysts to use as they looked for other biotech firms to buy.

“They had these investment bankers to make acquisitions, but we don’t have

capital to do acquisitions,” Morris says.

After the takeover, Morris and the board laid off the New York staff and

sublet the midtown office space, saving InfuSystem about $1 million a

year, Morris estimates. When he visits New York, Morris crashes on

George’s couch rather than charge the company for a hotel. These

cost-cutting moves helped InfuSystem post its first quarterly profit since

2010 in November. Yet Morris has more work to do—shares are still down

since he bought them.

Morris now spends about a third of his time on InfuSystem and the rest on

other investments. Knowing he’s not likely to see another market like

2009, he views activism as a way to get a persistent advantage in normal

times. “I think now he is struggling to say, How do I apply this? What

will allow me to be my own catalyst and allow me to find another edge?”

says Ashton. “Not in terms of size of return, but where I have an edge

that is somewhat durable.” Chris Cernich, executive director for proxy

contest research at Institutional Shareholder Services, has found that

companies with an activist investor on the board typically outperform

their peer groups by 16.6 percentage points. But activism, with its

patience and strategizing and expense, isn’t for most people, and the

battles don’t always end well.

In August, Morris saw a different activism project fall apart. He’d tried

to take over Pinnacle Airlines, a regional carrier, which later fell into

bankruptcy. After a judge denied Morris’s requests for more shareholder

input, Morris decided it wasn’t worth appealing the ruling. “Investing

isn’t a crusade, it’s about making money,” he says. Pinnacle became the

28-year-old’s biggest loss to date.

Around the same time, a friend who runs another small hedge fund tipped

Morris off to Lucas Energy (LEI),

a small energy producer with rights to drill on oil-rich properties but

not enough capital to get the crude out of the ground. It also had a CEO

and co-founder who was “not a great communicator,” Morris says. “I’m being

polite here.” After acquiring 11 percent of the company’s shares, Morris

flew to Texas to meet the CEO and chairman. He headed back the next day

with an invitation to have two seats on the board, with no strings

attached. Within three weeks, he and the rest of the board brought on a

new CFO, and in December they replaced the CEO.

Morris says he’s getting used to the ups and downs that are part of

long-term investing. He works out of a two-bedroom apartment in San

Francisco he shares with his “really supportive fiancé,” a blonde

Belarussian he met at a coffee shop in Santa Monica. “So that keeps me

sane,” he says. Plus: “My investors are very patient with me. I’m very

grateful.” Morris now has 33 investors and about $15 million under

management.

His long-term plan is to “cut my teeth with these small ones that I fix up

and sell, and then you can start doing more interesting strategic stuff

once you get bigger.” Eventually, he wants to merge companies, change

operations, and make the big plays. But to get there, Morris needs more

money, and more experience sitting across the table from executives and

demanding a seat on a board. It may require a new tie.

|

©2012

Bloomberg L.P. All Rights Reserved. Made in NYC |

|