JUNE 16, 2015

As Stocks Edge Higher, Buyback Programs Get Riskier

Companies like GE and Apple continue to repurchase shares in large

numbers. But these programs may get riskier.

By S.L. Mintz

|

|

PHOTO CREDIT: INSTITUTIONAL INVESTOR |

Few companies “go big or go home” with more gusto than Fairfield,

Connecticut’s General Electric. By announcing a $50 billion stock

buyback, the global industrial conglomerate joins yet another elite

club. Only Cupertino, California–based

Apple’s

buyback program, now pegged at an astounding $200 billion, exceeds the

scale GE has proposed. GE’s buyback commitment is five times larger

than its previous stock repurchases over the eight quarters through

the end of March. Subject to price fluctuations, GE expects to retire

up to 20 percent of its shares by the end of 2018.

The GE buyback is clearly tied to the company’s recent strategic

decision to sell its finance unit, GE Capital, a move that will

eliminate a big source of profits. Generating earnings per share will

be a challenge despite the agreement to acquire Levallois-Perret,

France–based power generation and distribution giant Alstom for $13.5

billion. The buyback, says analyst Steven Winoker at New York money

manager AllianceBernstein, “is meant to offset dilution associated

with the exit of GE Capital.”

GE highlights a stock buyback trend that has not significantly eased

even as pricier shares make so-called capital return programs, which

combine repurchases and dividend payouts, riskier. In the eight

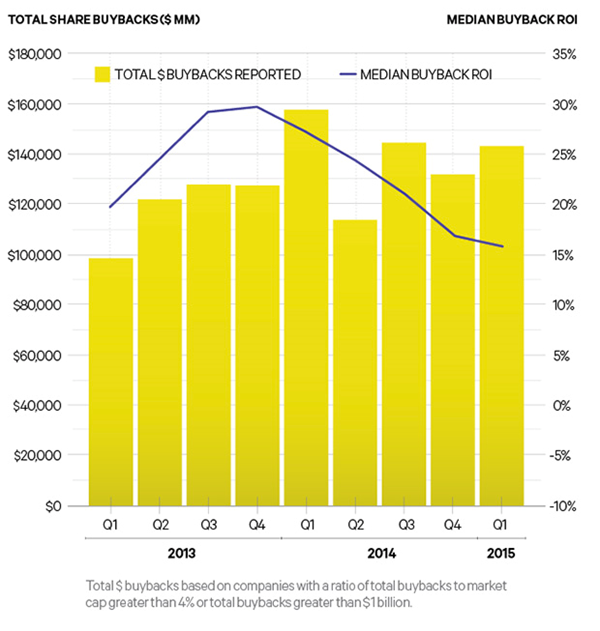

quarters through the end of March, some 276 companies in the Standard

& Poor’s 500 repurchased 4 percent or more of their market

capitalization. In the first quarter of 2015, buybacks approached $144

billion, a brisk pace, if just behind the $158 billion in the

first quarter of

2014. Since Institutional Investor initiated the

Corporate Buyback

Scorecard in 2013, companies meeting the 4 percent

threshold have diverted $1.2 trillion to buybacks, or a median $128

billion per quarter.

“S&P firms know that annual revenue growth is slowing at this late

stage in the cycle,” says John Blank, the chief equity strategist at

Chicago-based Zacks Investment Research. Slower growth prospects

combined with a strengthening dollar, growing piles of cash and low

borrowing rates contribute to the case for buybacks. “Buybacks are the

easy way to build up EPS when fundamentals are so soft,” he says.

“It’s probably a signal of both weak operating earnings growth and,

somewhat paradoxically, weak revenue growth performance.” The heart of

that paradox is when buyback volume exceeds earnings.

Although buybacks represent major corporate investments, their

announcements seldom stir much of a debate about accountability for

outcomes. This absence led to the creation of the Quarterly Buyback

Scorecard, developed by and computed for Institutional Investor

by Fortuna Advisors using data from S&P Capital IQ. Quarterly

scorecards look back two years to analyze whether buybacks rewarded

shareholders, or punished them, during that span. “It’s a very

legitimate question to ask,” says chief financial officer Dennis

Kelleher at CF Industries Holdings, a Deerfield, Illinois–based

fertilizer company, which has used buybacks to trim its market capital

by 23 percent according to the latest scorecard.

Companies continue to spend heavily to buy back shares. Nineteen

companies each repurchased more than $10 billion worth of stock in

this scorecard. The latest GE initiative, scheduled to be completed by

2017, exceeds its 2014 earnings by more than three to one and its 2014

capital expenditures by a similar margin. GE’s buyback performance,

however, has been lackluster over the past two years. Its repurchase

program generated a 4.6 percent return on investment, putting it at

No. 209 in 2015’s first quarter, down from No. 180 in the first

quarter a year ago. In the first quarter of 2013, GE ranked 82nd, with

an ROI of 26 percent.

Volume, timing and motives differentiate individual buyback programs.

Some companies want to absorb excess shares in the wake of

divestitures or shares issued to facilitate acquisitions. Cincinnati

supermarket chain Kroger Co. has a long record of using cash flow from

its stores to repurchase shares ever since it issued new shares in

1999 to merge with the Fred Meyer chain. “We started a buyback program

to reduce dilution,” Kroger chief financial officer J. Michael

Schlotman told Institutional Investor in 2014. At 71 percent

ROI, Kroger currently ranks No. 3 in buyback ROI.

Apple’s buybacks

served to placate activists like Carl Icahn and others who saw few

better uses for the company’s huge amount of cash. The most recent

scorecard shows that those buybacks have produced stellar results. Two

years ago Apple’s buyback ROI was in the basement. But in this

scorecard the company records the sixth-best ROI, at 54 percent.

Apple’s buyback ROI exceeded its buyback strategy, a proxy for total

return to shareholders, by 12 percent.

Buybacks often beget more buybacks. Apple recently announced a plan to

boost its capital return program from $130 billion to $200 billion by

March 2017.

Not everyone has performed as well as Apple, with an uncertain market

taking its toll. In the first-quarter scorecard, median two-year

buyback ROI for the S&P 500, in which companies retired at least 4

percent of market capital, ticked down from the previous quarter by

one percentage point, to 16.5 percent. A year ago median buyback ROI

for the S&P buyback cohort was 25.2 percent, off its peak of 26.8

percent at the end of 2013.

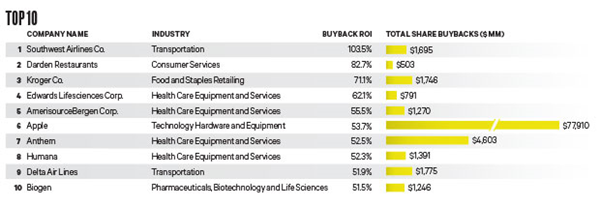

Current scorecard leader Dallas-based Southwest Airlines repurchased

shares in all eight quarters, from a low of $39 million in the fourth

quarter of 2013 to $315 million the following quarter. All told,

Southwest bought back shares worth $1.7 billion, or 5.7 percent of its

market capital. The investment nearly doubled in value, to $3.3

billion.

No. 2 on this quarter’s scorecard is Orlando, Florida–based Darden

Restaurants, which owns and operates more than 1,500 family-style

restaurants. Darden, which has been the target of hedge fund activist

campaigns, deployed a portion of the proceeds from the sale of its Red

Lobster chain to buy back shares. An accelerated repurchase program

took shares off the hands of two institutional investors, Goldman

Sachs and Wells Fargo Bank. Buyback ROI at Darden surpassed 82

percent.

Some buybacks, like Darden’s, are intended to mollify activists,

whereas others grease the wheels of strategic alliances. For example,

buybacks helped Bethlehem, Pennsylvania, drug distributor

AmerisourceBergen Corp. ink a purchasing pact with Deerfield,

Illinois, drug retailer Walgreens Boots Alliance. Terms of the deal

allowed Walgreens to buy 7 percent of AmerisourceBergen plus warrants

amounting to 16 percent of the drugstore company’s outstanding shares,

exercisable between March 2016 and September 2017. Anticipating

potential dilution when warrants are exercised, notes analyst Ann

Hynes at Mizuho Securities, AmerisourceBergen began repurchasing

shares. So far, the company’s timing has been excellent, and it ranks

No. 5 on the current scorecard.

Three other health care equipment and services companies join

AmerisourceBergen at the top of the scorecard: Irvine, California,

heart valve manufacturer Edwards Lifesciences (No. 4) and managed care

health insurers Anthem (No. 7), based in Indianapolis, and Humana (No.

8), headquartered in Louisville, Kentucky. Humana announced a $2

billion buyback in September 2014 after reporting a dip in net profit

as benefit costs increased.

Atlanta’s Delta Air Lines (No. 9) and Cambridge, Massachusetts,

biotech Biogen (No. 10) fill out the top tier.

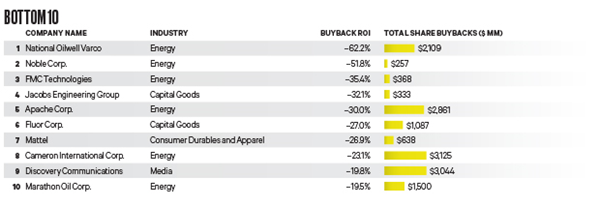

At the other end of the ranking are two capital goods companies, a

media company and a consumer durables and apparel retailer. Four

energy companies ended up in the basement as well, hurt by the slump

in oil prices. In dead-last place Houston-based oil and gas equipment

supplier National Oilwell Varco saw its repurchased shares lose 62

percent. One spot above, London-based Noble Corp., a contract oil and

gas driller, lost 52 percent. By contrast, Tesoro Corp., a San

Antonio, Texas–based refiner, ranks at No. 11 with a buyback ROI of 51

percent.

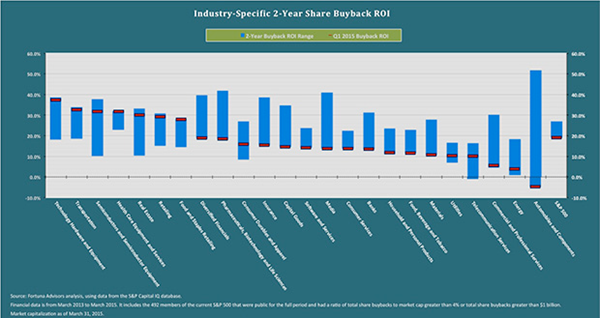

For the past two years, six sectors come in near the top of their

buyback ROI ranges and 14 are near their bottoms, with a handful —

telecom services, utilities, and consumer durables and apparel —

somewhere in the middle. Technology hardware and equipment,

transportation, and food and staples retailing still show strength.

But with so many sectors near their lows, the S&P 500 in the latest

scorecard languishes near the bottom of its ROI range.

In this scorecard a median company retired shares equivalent to 6.7

percent of its market capital. Buybacks at 13 retired more than a

fifth of market capital. One of the latter is CF Industries, at No.

47, which bests all but two of 15 companies in the materials sector,

beating the median ROI in its peer group by two to one.

Buyback strategy at CF is part of a rigorous approach in managing a

global competitor in the manufacturing and distribution of

nitrogen-based fertilizer products. “We really think of this as a

machine in trying to grow cash generation through nitrogen capacity

per share,” Kelleher says.

A string of buybacks in combination with new revenues from

acquisitions tested CF’s metric. CF now generates 143 tons of nitrogen

capacity per 1,000 shares of stock, a three-fold increase since 2010.

A market climate favorable to buybacks can override earlier guidance

from the company. CF had warned analysts to anticipate a pause in

buybacks during the first quarter of 2015. When conditions

unexpectedly favored buybacks in that period, CF returned to the

market. “We took the view that we had a good handle on cash flow, knew

where we were going and that it made sense to be in the market after

saying we would not be in the market,” Kelleher says.

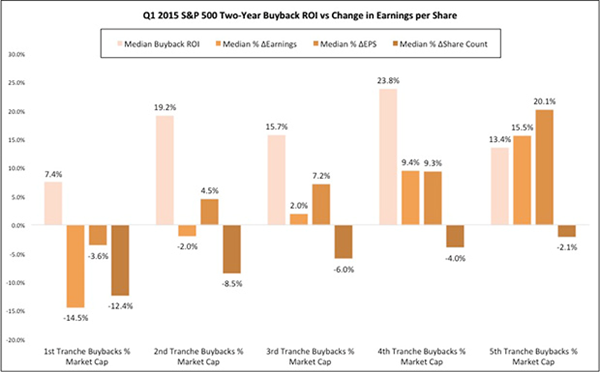

No matter what motivates companies, buybacks share a common effect: As

the number of shares falls, EPS tends to rise. In the current

scorecard Fortuna analyzed this relationship by matching buyback ROI

quintiles with changes in EPS. Overall, the data confirms what we

expected: Buyback ROI and EPS generally move in tandem. The top

tranche in median buyback ROI recorded the top median percentage

change in EPS. Lower tranches behaved similarly, with the fifth

tranche recording the lowest median percentage change in EPS.

That’s a general observation that applies to companies in aggregate.

Results for individual businesses are more difficult to predict.

Houston’s Cameron International Corp., a supplier of measurement and

control equipment for oil and gas producers, repurchased almost a

fourth of its shares, a higher percentage than any other company in

the current ranking, over the eight quarters through the end of March.

Nonetheless, its EPS slid by more than 57 percent as buyback ROI took

a pounding, falling by 23 percent.

Grouping companies in buyback ROI quintiles highlighted similar

reductions in share count. However, the median change in EPS for each

group fell sharply descending through the quintiles. In the top

buyback ROI quintile, a median company reduced share count by 6

percent and posted a 36 percent increase in EPS and 40 percent buyback

ROI. The bottom quintile did not feature aggressive buybacks as a

rule. The median company in that group bought back 6 percent of its

shares but posted an 11 percent decline in EPS and an 8 percent slide

in buyback ROI. Instead of signaling good news, buybacks at a fifth of

the companies signaled that they would be generating lower EPS in the

future.

Across the board, companies hoping to improve market performance or

EPS with buybacks, rather than by growing the business, will often

find the going rough. As Fortuna CEO Gregory Milano concludes: “Our

study showed that EPS growth from buybacks added about half the value

versus EPS growth from operations.” Operations still matter.

|

© 2015 Institutional Investor LLC. |

|