|

THE

WALL STREET JOURNAL.

|

Markets

Deals & Deal

Makers

Wall Street Law Firms Challenge Hedge-Fund Deal Tactic

Lawyers take issue with ‘appraisal arbitrage’ strategy

By

Liz Hoffman

Updated April

6, 2015 8:53 p.m. ET

A group of large Wall

Street law firms have banded together in an unusual bid to clamp down

on a popular hedge-fund strategy aimed at squeezing more money from

corporate takeovers.

Seven firms—including

Cravath, Swaine & Moore LLP; Davis Polk & Wardwell LLP and Latham &

Watkins LLP—are urging changes to rules governing an “appraisal,” a

legal move in which stockholders who feel shortchanged by a takeover

seek a higher valuation.

The firms made their case

in a letter sent last week to a group of Delaware lawyers charged with

recommending changes to the state’s corporate code, which governs the

vast majority of U.S. public companies. A copy of the letter was

reviewed by The Wall Street Journal.

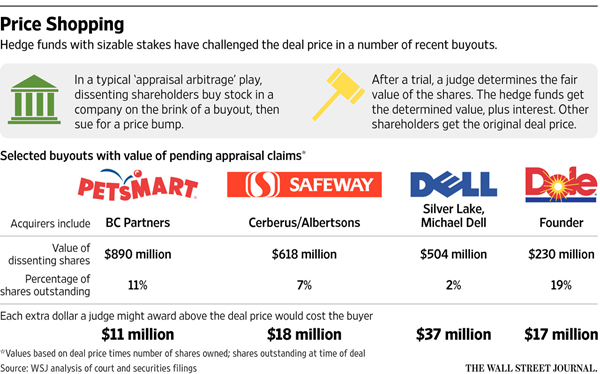

The backdrop for the push

is a sharp rise in so-called appraisal arbitrage, in which funds buy

shares of a company on the brink of a sale and argue it is worth more

than the takeover price. A record 33 public-company appraisal cases

were filed last year in Delaware, and another 20 have been filed in

2015, according to a Wall Street Journal analysis. The targets are

often private-equity-backed buyouts, with both of the largest such

deals agreed to last year being challenged, those for grocery-store

chain Safeway Inc. and retailer PetSmart Inc.

The law firms that signed

the letter are some of the biggest names in mergers and acquisitions.

Among their top clients are private-equity firms and target companies,

which generally oppose appraisal arbitrage, as it threatens to

complicate their deal making and make it less lucrative.

The issue is likely to

come to a head by June 30, when the Delaware legislative session ends.

Delaware law allows

investors seeking appraisals to buy shares right up until a deal

closes, after the voting-eligibility deadline known as the record

date. Critics argue the setup leads to an abuse of the appraisal

right, which they say was meant to protect long-term shareholders from

being taken advantage of in a merger. Also encouraging funds to mount

the campaigns: They are guaranteed interest equivalent to 5.75%

annually on the value of their stakes as the appraisal review takes

place. That amount, established during a period of higher interest

rates, is especially attractive amid today’s low yields.

The New York firms want to

deny appraisal rights to funds that buy shares after the record date,

according to the letter, which is also signed by Skadden, Arps, Slate,

Meagher & Flom LLP; Simpson Thacher & Bartlett LLP; Sullivan &

Cromwell LLP and Wachtell, Lipton, Rosen & Katz.

Such a change would

“reduce the unseemly claims-buying that is rampant and serves no

legitimate equitable or other purpose,” the letter said. The threat of

an appraisal could lead acquirers to bid less upfront, knowing they

may be forced to pay more later, the letter added.

The proposal goes further

than one proposed by the group reviewing potential changes, whose

recommendations are typically approved by the state legislature with

little pushback.

A lot is at stake for the

companies in question. Hedge funds including

Fortress Investment Group LLC and

Magnetar Financial LLC are seeking appraisal for some $230 million of

shares in Dole Food Co., whose case is pending a decision. They are

looking for nearly twice the $13.50-a-share the company’s chairman

agreed to pay in his 2013 buyout of the firm, which was valued at $1.2

billion.

Some deals have attracted

even bigger bets. Hedge funds including Third Point LLC have nearly

$890 million tied up in claims challenging the roughly $8.25 billion

buyout of PetSmart. It isn’t clear yet how much the funds will seek

above the $83-a-share price a private-equity group agreed to pay for

the company late last year.

Write to

Liz Hoffman at

liz.hoffman@wsj.com

|