|

Analysis

Appraisal Arbitrage Dimmed By

Delaware Rulings

By

Chelsea Naso

Law360

(February 15, 2019, 4:07 PM EST) -- Appraisal arbitrage is falling out of

style as the reality of recent Delaware rulings sets in, with a new study

showing the number of mergers facing shareholder challenges over deal

price dropped meaningfully for the second year in a row.

A study from

Cornerstone Research released

Wednesday evaluates how appraisal litigation has evolved since a 2007

opinion in In re: Appraisal of Transkaryotic Therapies Inc. laid the

groundwork for an investment strategy known as appraisal arbitrage. The

strategy sees shareholders — largely hedge funds and private equity firms

— buy into target companies with the goal of gaining a higher deal price

for their shares through the court.

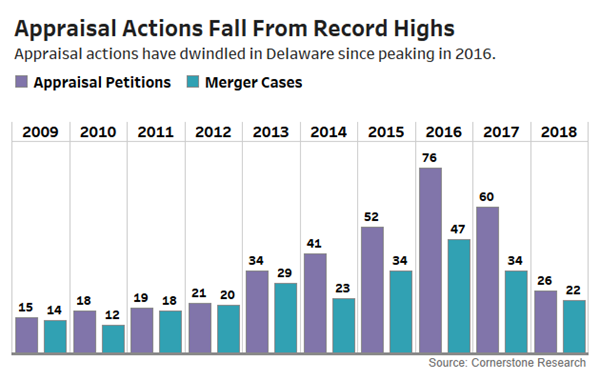

The study found that the number of mergers facing appraisal actions fell

to 22 in 2018, marking the second year of decline after peaking at 47 in

2016. That rapid slide coincided with a drop-off in the overall number of

appraisal petitions filed. There were 26 appraisal petitions filed in

2018, down from 60 in 2017 and 76 in 2016, according to the report.

Two

opinions from the Delaware Supreme Court weighing in on the private

equity-backed buyouts of payday lender DFC Global Corp. and technology

giant

Dell Inc. are viewed as somewhat of a

turning point for appraisal arbitrage because of the emphasis placed on

deal price as a strong gauge of fair value.

“From my view, it’s because of the significant development in appraisal

law in the last few years culminating in two Supreme Court cases, DFC and

Dell, which effectively made clear that deal price may well be the best

indicator of fair value in appropriate circumstances,” said Edward

Micheletti, head of

Skadden Arps Slate Meagher & Flom LLP’s

Wilmington, Delaware litigation practice.

In the DFC case, the Delaware Supreme Court in August 2017 overturned the

Chancery Court’s determination that the payday lender’s private equity

buyer had underpaid by about $100 million of the $1.3 billion acquisition.

The 87-page opinion penned by Chief Justice Leo E. Strine Jr. said that

best evidence of fair value in the DFC case was indeed deal price, but

declined to create a broad judicial rule that would apply deal price in an

appraisal of an arm’s length transaction.

The Delaware Supreme Court in December 2017 also reversed a Chancery Court

decision that had found that Dell’s $25 billion buyout was underpriced by

roughly $7 billion. In an 84-page decision penned by Justice Karen L.

Valihura, the justices remanded the case back to the Chancery Court,

directing Vice Chancellor Laster to either appraise the transaction at its

deal price with no further proceedings or choose “another route” based on

the Delaware Supreme Court’s findings and explain his reasoning. The

justices took particular issue with Vice Chancellor J. Travis Laster’s

decision to give no weight to the deal price.

“Dell and DFC basically said that where you have an appraisal case

following a competitive sales process, the transaction price should be

given strong weight, and it should be the factor that is weighed most

heavily in those cases,” said David Hennes, co-chair of

Ropes & Gray LLP’s corporate and

securities litigation practice.

There have also been a number of decisions in 2017 and 2018 that found the

fair value to be below deal price, shaking shareholders’ confidence that

they will be able to get more cash for their shares.

The rulings in appraisal cases of

Clearwire Corp.,

PetSmart Inc.,

SWS Group Inc.,

Solera Holdings Inc.,

AOL Inc. and Aruba Network Inc. all

drew rulings that pegged fair value below the deal price.

“The risk to petitioners is that now we are seeing results below the

transaction price and, if that occurs, petitioners are going to take a

loss on those investments,” Hennes said.

The structure of the sales process seems to be a key factor in the outcome

of appraisal cases, the Cornerstone Research study found. According to the

study, appraised transactions that included an auction process or a

go-shop period saw the average premium to deal price land at 1 percent

while appraised transactions without those factors where the acquirer was

a related party saw an average premium of 47 percent awarded to the

petitioners.

The study also found that of the 34 cases that went to trial between 2006

and 2018, 16 challenged transactions were appraised above the deal price

while the other 18 came in at or below the deal price.

The highest premium — 158 percent — in the time frame was secured in 2016

by the shareholders who challenges the acquisition of INS Software Corp.

And the biggest hit to premium — negative 57 percent — was seen in the

challenge to Sprint’s acquisition of Clearwire following a bidding war.

While some of these closely watched cases have placed an emphasis on

giving weight to deal price, that’s just one of a handful of methods that

the Delaware courts use when tasked with determining the fair value of a

company in an appraisal action.

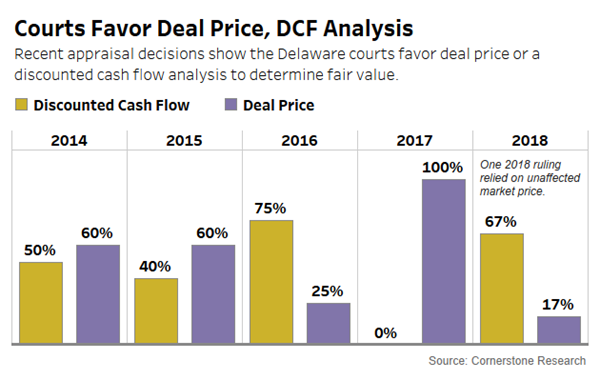

In the 13 years covered by the Cornerstone Research study, the Delaware

courts relied on a discounted cash flow analysis — a method of determining

a company’s current value that incorporate future cash flows — 59 percent

of the time and relied on deal price 38 percent of the time. The courts

never based fair value on the value of comparable companies or precedent

transactions during the time frame. And in 2018, for the first time, the

Delaware Chancery Court in its

appraisal of Aruba tied fair value to the company’s unaffected market

price.

The

Aruba case saw Vice Chancellor J. Travis Laster — the same justice who

penned the Chancery Court’s Dell ruling — in February slash 30 percent

from Hewlett-Packard Co.’s $2.8 billion takeover of Aruba when he used the

target’s unaffected 30-day average market price to determine fair value.

In the 129-page opinion, Vice Chancellor Laster said that “forceful

discussions” in the Dell and DFC opinions about reliance on valuations

based on efficient capital markets justified giving market value

substantial weight.

Delaware’s Supreme Court has yet to weigh in on the case.

--Additional reporting by Jeff Montgomery. Editing by Alanna Weissman.

© 2019, Portfolio Media, Inc. |