|

THE WALL STREET

JOURNAL. |

MARKETS

|

Deals & Deal Makers

First Rule of

Mergers: To Fight Is to Lose

Shareholders Challenged 94% of U.S.

Public-Company Deals Last Year

|

|

By

Liz Hoffman

March 26, 2014 12:06

p.m. ET

Corporate mergers are often fraught with uncertainty over whether the

deal will succeed, culture clashes between the two companies and the

fate of executives.

But two things are virtual locks: The companies will get sued by

shareholders unhappy with some aspect of the deal, and eventually they

will settle with the offended parties without significant changes to

the transaction.

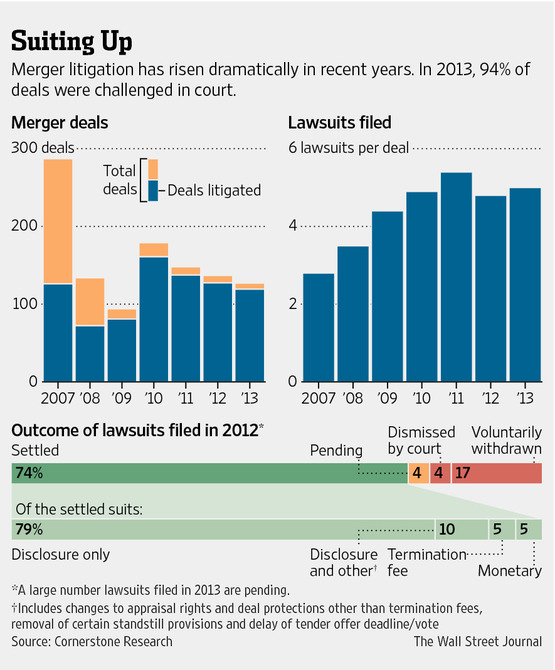

Shareholders challenged 94% of U.S. public-company deals last year, up

from 44% in 2007, according to Cornerstone Research, a litigation

consulting firm. The average deal now faces five lawsuits, often filed

in different state and federal courts.

Lawsuits are among the weapons at shareholders' disposal to hold

boards accountable. But the recent proliferation of legal actions has

diluted their power, people on both sides of these cases say.

"It's a classic case of crying wolf," said Sean Griffith of Fordham

University School of Law. "If the goal of the legal system is to add

value for shareholders, it's failing."

When

Cisco Systems Inc. agreed last July to buy software company

Sourcefire Inc., the first shareholder lawsuit came within three days,

alleging the price was too low. Three more followed in state and

federal court.

The cases settled six weeks later, with Sourcefire agreeing to tell

shareholders more about the deal, including how its bankers deemed

Cisco's $2.7 billion offer fair. It also agreed to pay $400,000 to the

plaintiffs' lawyers. Shareholders got no additional money. The deal

closed in October.

The vast majority of these cases settle as Sourcefire's did, with no

bump in the deal price. Instead, companies agree to disclose more

details and pay shareholders' attorneys' fees, which averaged $500,000

last year, according to Cornerstone. In return, they can close their

merger without the threat of a long court battle.

"It's Kabuki theater," said Robert Daines, a former

Goldman Sachs Group Inc. banker and now a professor at Stanford

Law School. "Everybody knows the moves."

Critics say the system benefits plaintiffs' lawyers, who collect

hundreds of thousands of dollars in fees, and defendant companies, who

get peace of mind for what amounts to a rounding error in deals that

often are valued in the billions.

It is almost always cheaper and less risky for companies to settle,

especially when facing lawsuits in multiple courts. One unfavorable

ruling can derail a deal for months.

The one group that usually doesn't benefit, at least financially, is

shareholders. Out of more than 380 challenged deals since 2011, only

four—about 1%—yielded more money for shareholders in court, according

to Cornerstone. Some critics warn the increase in litigation actually

may hurt shareholders by burying real cases of misconduct in a flood

of filings. "Some good suits get missed," Leo E. Strine, Jr. , chief

justice of the Delaware Supreme Court, wrote in a paper last year.

In some lawsuits, judges have found troublesome behavior. El Paso

Corp. paid investors $110 million after a judge found that conflicts

of interest among the company's management and bankers likely tainted

its 2012 buyout. Similar claims in the 2011 sale of Del Monte Foods

yielded nearly $90 million for shareholders. Neither company admitted

wrongdoing.

Just this month, a judge found that RBC Capital Markets LLC

manipulated the 2011 sale of ambulance operator Rural/Metro Corp. in

an effort to win more fees for itself, a decision that could hand

shareholders millions of dollars. RBC has said it acted properly and

is weighing its options.

Plaintiffs' lawyers note that in other countries, government

regulators review deals for fairness. In the U.S., "nobody is looking

out for shareholders except lawyers," said Mark Lebovitch of Bernstein

Litowitz Berger & Grossmann LLP, which represents investors.

Still, even some defenders of the system say it can and should work

better.

"The plaintiffs' bar has swung too far, and that's a problem," said

Stuart Grant, who represented shareholders of El Paso and Del Monte.

"It hurts shareholders who have good cases."

The flood of filings may be creating odd incentives. Some critics of

companies allege they are deliberately withholding deal details to

have fodder for quick settlements.

The issue cropped up in the recent sale of Mako Surgical Corp. to

Stryker Corp. Mako’s financial projections were missing from the

preliminary packet of information sent to shareholders. Courts

generally have said shareholders are entitled to these numbers.

Plaintiffs' lawyers accused Mako of deliberately holding back the

projections to be able to disclose them later to settle the case. "For

them to play 'hide-the-ball' with the shareholders like this is really

gamesmanship," lawyer Donald Enright said at a November hearing. The

deal closed in December, after Mako made additional disclosures and

agreed to negotiate a "reasonable" fee for Mr. Enright's firm and

others.

Similar claims have been made in other cases. Some have found

sympathetic judges frustrated by what they see as tactical holdbacks.

"You create this situation where the bankers have an incentive to not

put in this stuff," J. Travis Laster, a judge in Delaware's business

court, said in a 2011 hearing.

Some judges have been pushing back against suits they deem frivolous.

The average fee awarded to plaintiffs' lawyers has fallen by nearly

half since 2008, according to Cornerstone.

In other cases, judges have rejected disclosure-only settlements.

Judge Strine in February refused to approve such a settlement over the

sale of Medicis Pharmaceutical Corp. The plaintiffs' lawyers were

seeking $400,000, which Medicis had agreed to pay. But Judge Strine

said the plaintiffs' lawyers hadn't uncovered any problems with the

transaction. "I think at some point in time, you have to candidly say,

'We struck out,'" he said in court.

Write to

Liz Hoffman at

liz.hoffman@wsj.com

|