|

Forum Report:

HC2 Shareholder Survey

2019 Survey of HC2 Holdings, Inc. Shareholders

Value enhancement alternatives

Management of favored alternative

Comments presented for the company’s consideration

Shareholder comments for other shareholders

Shareholders of HC2 Holdings, Inc. were invited to report their views of

management alternatives during the week following September 10, 2019.

The

survey research was initiated by HC2 shareholders seeking an understanding

of what strategies other shareholders would support to establish marketplace

valuations of the company’s stock in a range consistent with reported

professional valuations of the company’s subsidiary holdings.

The

survey questionnaire also asked participants to volunteer information that

might be useful in analyzing anonymous responses, about what kind of

portfolio(s) they managed, how many shares they owned, how long they had

owned shares, and whether they had recently increased or decreased their HC2

investment. Participants were also offered an opportunity to present

questions or comments anonymously for the Forum to report for consideration

by HC2’s management or other shareholders.

Value

enhancement alternatives

The

initial issue shareholders were invited to address was to “how much you

believe each of these alternatives would contribute to the value of your HC2

stock,” presenting a list of specified strategies and offering an

opportunity for respondents to write in their own suggestion of an “other”

alternative.

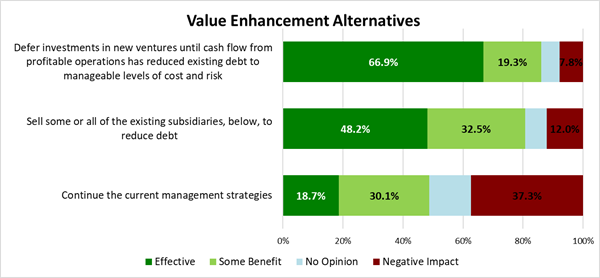

As

shown in the following graph, the highest level of shareholder support was

for the alternative to “[d]efer investments in new ventures until cash flow

from profitable operations has reduced existing debt to manageable levels of

cost and risk,” with 86% of respondents believing that would be effective or

provide some benefit. The next highest level of support was for the similar

alternative of selling some or all subsidiaries to reduce debt, with 81% of

respondents believing that would be effective or provide some benefit.

Support for specific disposition alternatives ranged from 69% to 53%, except

for the strongly opposed sale of the Construction Group which was supported

by only 38% and received the highest level of perceived negative impact by

44% of shareholders. Most significantly, fewer than half of the responding

shareholders thought a continuation of current management strategies would

be effective or at least provide some benefit, and more than a third thought

it would have a negative impact.

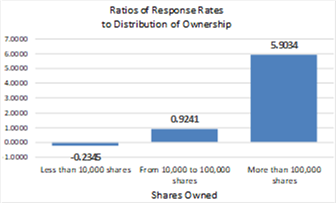

It

should be noted that these patterns of support for both deferral of new

venture investments and sales of subsidiaries to reduce debt were much

stronger among respondents reporting ownership of more than 100,000 shares.

Most significantly, more than two thirds of those larger shareholders

reported believing that a continuation of current management strategies

would have a negative impact.

Comments offered by shareholders addressing this question were generally

consistent with their choices of alternatives, as shown in this range of

examples:

■

act

fast

■

bring

in operator to run company properly, stop new projects, significantly cut

G&A

■

liquidate

■

manage

debt as we move into the downturn. rates will be even lower then if more

borrowing is needed

■

management could try to reduce corporate overhead expenses as currently they

are too high (25-30mn per yr) given the tight free cash flow situation

■

Most

of these questions depend on price. So it is tough to say on just a blanket

should we sell this asset, it depends on the sure, sure sell DBM if you can

get 2 billion.. I was unaware there were issues with NY for Continental

■

Something must be done to address staggering debt and excess management comp

■

The debt level is too high given the cash flows of the combined operations.

■

There

are too many assets that are not cash flow positive, and the corporate

overhead costs are too high given the underlying assets of the business

Management of favored alternative

Following the question above about strategy alternatives, participants were

asked “[f]or whichever alternative(s) you consider most likely to be

effective, how do you think the value enhancement process could be most

reliably managed?”

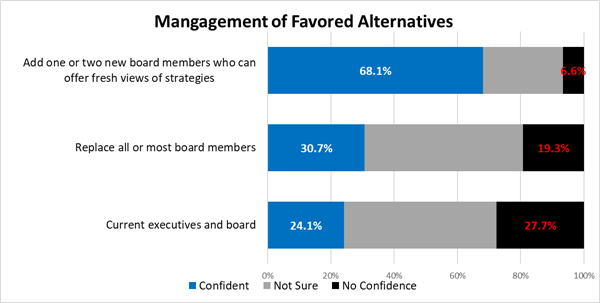

Understandably in the context of support for change, most shareholders

reported that they would have confidence in the management of their favored

alternative if there was at least some change in HC2’s board of directors.

The strongest support, with 68% expressing confidence and only 7% lacking

confidence, was for the relatively safe addition of one or two new board

members to provide fresh views. However, as shown in the graph below,

significantly more shareholders had confidence in a new board than the

number who lacked confidence in that more pivotal change of management.

Consistent with that response, the number of shareholders who lacked

confidence in HC2’s current board and executive management was greater than

the number of shareholders who expressed confidence in them.

As in

their responses to alternative strategies, respondents reporting ownership

of more than 100,000 shares showed much stronger views. More than two thirds

of these larger shareholders expressed both confidence in a replacement of

all or most board members and a lack of confidence in the current executives

and board.

Comments offered by shareholders addressing management included a range of

views shown in these examples:

■

Add

some one from Steel Partners (they own 1,000,000 shares)to your board, they

know how to create value

■

Company was highly rated a few years ago as a potential 100x gain over time.

Use successful actions that created your promising future and continue to

build you team for success

■

Current management is a disaster and they should be replaced. The Board

should have quit after the say on pay vote and the current board is a

disgrace.

■

I

think the stock price speaks for itself as far as investor confidence in

management.

■

liquidate save 25mm overhead

■

Maybe

you should seek out a really smart activist investor rather than waiting for

them to come find you in a hostile manner. For example reach out to Icahn

and see if he is interested in taking a stake.

■

New

directors without past history with ceo

■

Please

operate with more integrity. DO NOT lie to your shareholders for three years

about “top priority” and then do the opposite; sell assets and use no

proceeds to tackle your investors concerns. Management has been negligent

with leverage at the holding company, they have leveraged the company to

such an extent that it now makes selling assets for a fair price next to

impossible. Global has been for sale almost a year now, potential buyers of

the asset are aware of the high levels of debt and leverage that the holding

company, and are using that to their advantage. We will be forced to unload

the asset at a sub optimal price due to managements negligence with

leverage. It is downright repulsive the way Phil and co. have conducted

themselves since the inception of Hc2 holding. Take zero pay until you

create shareholder value, you have robbed your investors for the past number

of years with exorbitant bonuses for costing your shareholders significant

losses.

■

Some

continuity of management necessary, but fresh eyes valuable.

■

The

Board are all yes-men to Falcone. They need to be replaced

■

The

reports on management that I've read are quite positive. Looking forward, as

long as people with excellent skills and experience are guiding the company,

the pursuit of steady, stable growth should go according to plan.

■

yeah,

fire falcone! no confidence.

Comments presented for the company’s consideration

Responding shareholders were invited to present comments and questions for

HC2 management, as well as suggestions of subjects for future company

reports or conference call presentations, with the assurance that their

responses would be presented to the company with sources identified only as

anonymous participants in the survey. The following reports of all responses

were presented to the company’s chief executive officer on September 18,

2019, the day after the one-week survey was closed:

·

Shareholder Suggestions for Management Consideration

·

Shareholder Questions for Company Management

·

Shareholder Suggestions of Subjects for a Company Report

HC2

management responded to these comments on September 25, 2019, with the

following statement:

|

HC2 Holdings, Inc. appreciates the concerns of our investors,

particularly with respect to our balance sheet. De-levering the

holding company remains our top priority. While the sale of Global

Marine is clearly at the forefront of this process, we continue to

evaluate additional paths with our other global portfolio companies.

As we show progress in improving our balance sheet, we believe

investors will be able to see the value we are creating and the

benefits of a diversified portfolio. We remain well-positioned to

take advantage of our diverse hybrid portfolio strategy of solid cash

generating businesses such as Construction, Insurance and meaningful

value creation at Global Marine, Energy, Broadcasting and Life

Sciences. |

On

September 26, 2019, the company also replaced its investor relations website

presentation of a November 2018 “Corporate Overview” with a new “Investor

Presentation” supporting their statement in response to the survey comments.

Shareholder comments for other shareholders

The

questionnaire also invited shareholders to offer comments for consideration

of other HC2 shareholders, with the understanding that responses would be

similarly reported as presented by anonymous participants in the survey. All

of these comments are presented in the following report:

·

Comments Offered for Reporting to Other Shareholders

ttt

This

summary is being distributed to all shareholders who participated in the

survey and requested a report of its results, with thanks for their

contributions of views to benefit other shareholders and the company’s

management. Questions and comments about the survey results are welcomed,

and can be addressed to

hchc@shareholderforum.com.

GL

– September 27, 2019

Gary

Lutin

Chairman, The Shareholder Forum

©The Shareholder Forum, Inc. |