|

Forum

distribution:

Professional views of processes for investor access to

decision-making information

|

|

For the full report on which the article

below is based,

see

|

|

Source:

The Harvard Law School Forum on Corporate Governance and Financial

Regulation, February 19, 2019 posting |

Communicating with the Investment

Community in the Digital Age

Posted by Jonathan Doorley, Brunswick

Group LLP, on Tuesday, February 19, 2019

|

Editor’s Note:

Jonathan Doorley is partner at Brunswick Group LLP. This post

is based on his Brunswick memorandum. |

Having a sophisticated

and current understanding of how the investment community gathers and

processes information is critical for success when a corporate issuer

is communicating with the market on an ongoing basis or during a

complex situation such as a transaction or responding to a shareholder

activist.

Brunswick has been tracking the digital consumption habits of

institutional investors and sell-side analysts around the world for a decade,

and the results of our latest study reveal important trends that should be

considered when formulating both ongoing and event-driven investor engagement

programs.

Data Collection Methodology

In the fourth quarter of 2018, Brunswick’s in-house research

division (Brunswick Insights) surveyed 318 institutional investors (52%)

and sell-side analysts (48%) on their use of digital and social media platforms

in the investment research process. 40% of participants were located in the

U.S., with the remaining located throughout Europe, the U.K., and Asia. In this

report, “digital” refers to any information source, publisher or platform that

lives solely online, and “social media platforms” refer to a subset of digital

sources where users can consume, share and discuss information.

Highlights of Results

-

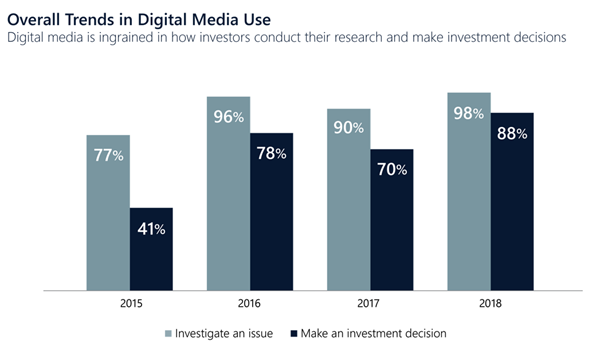

Use of digital research methods is now ubiquitous—According

to our study, 98% of the investment community uses digital sources to

investigate and conduct research during their investment process. 88% of

participants told us that they make decisions based on information they

learned online, marking a significant 18% increase from the 2017 results and a

41% increase from 2015.

-

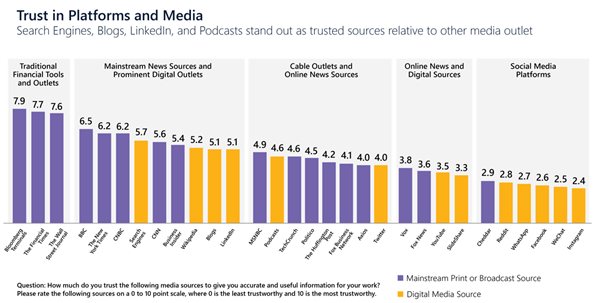

Trust in digital platforms is accelerating—The

investment community is placing increasing levels of trust in information that

they’re sourcing online. Though not quite at the same level as the most

top-tier financial media, trust levels for digital platforms now compare

favorably to other traditional content publishers. For example, information

from search engines is trusted on a similar footing with The New York Times,

CNBC and CNN. And the top social networking platform, LinkedIn,

is more trusted than MSNBC, TechCrunch and Politico. It’s

no surprise then that 81% of participants rely upon information retrieved from

Google during the research process and 63% of participants use LinkedIn for

the same purpose.

-

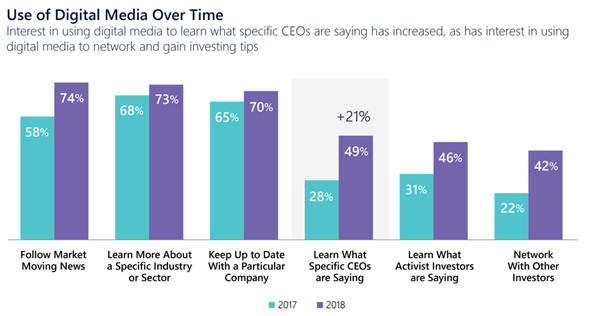

CEOs are expected to be digitally engaged—The

expectation for CEOs to engage with audiences via digital channels is

intensifying. Half of participants told us that they now use digital channels

to learn what CEOs are saying, a dramatic 21% increase over last year’s

results. That increase is especially significant among sell-side analysts, 59%

of whom now say that they use digital to stay connected with CEOs.

Key Recommendations for

Corporate Issuers

-

Utilize all available channels at your disposal—Over

the last decade, engaging with the investment community has evolved from a

quarterly or annual exercise managed by the investor relations department to

an ongoing strategic imperative that demands participation from senior

management and independent directors. While nothing will replace the core

tenants of a robust investor engagement program—roadshows, conference

participation, AGMs, etc.—digital channels provide an opportunity for

corporate issuers to communicate directly with investors and analysts on an

ongoing basis as well as around times of significant change like an M&A

transaction.

-

CEOs need to get in on the action—Executives

who lack a strong, personal digital profile and content strategy are creating

business risk. As a practical matter, building an effective individual digital

profile is not just an essential component in a successful investor relations

strategy, it is now a necessity for maintaining shareholder value and

competing with peers that are more active in digital and social media.

Concerns about Reg-FD issues and other SEC disclosure obligations are easily

mitigated through careful planning alongside legal counsel.

-

Don’t leave anything to chance—With

recent studies suggesting that corporate reputation is now directly

responsible for up to half of market capitalization, a robust and thoughtful

engagement strategy with the investment community—around results, off-cycle,

or event-driven—is critical for both maintaining and enhancing shareholder

value.

|

Harvard Law School Forum

on Corporate Governance and Financial Regulation

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2019 The President and

Fellows of Harvard College. |

|

|

|